The Covid Impact on Private & Alternative Credit in Europe

Post by : admintegeradvisors | Post on : June 19, 2020 at 2:10 pm

Navigating the Unknown

Covid Impact on Alternative Credit_Integer Advisors (PDF Version)

Covid Impact on Alternative Credit_Integer Advisors (PDF Version)

Executive Summary

The following is an excerpt of our report (see PDF link for full version)

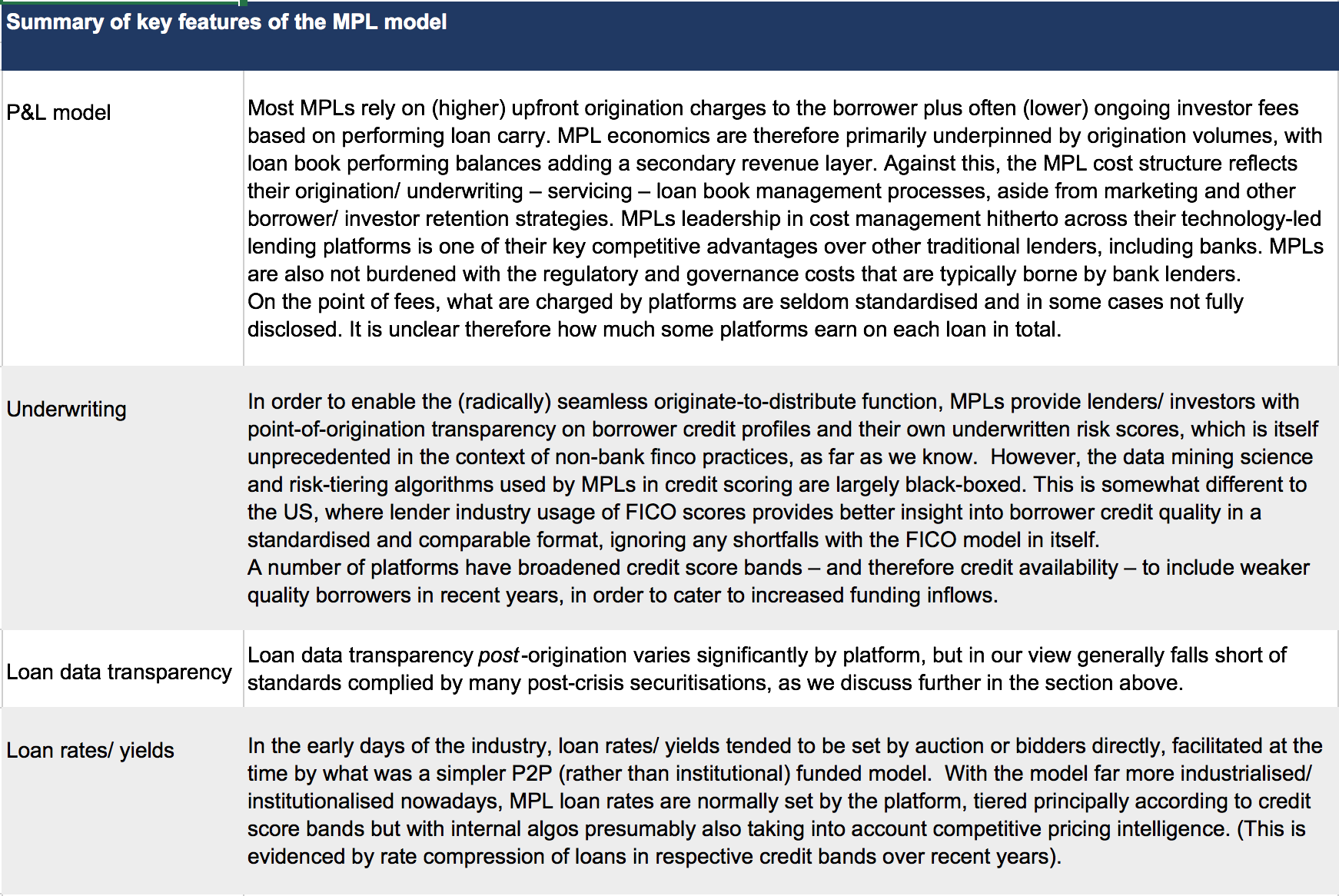

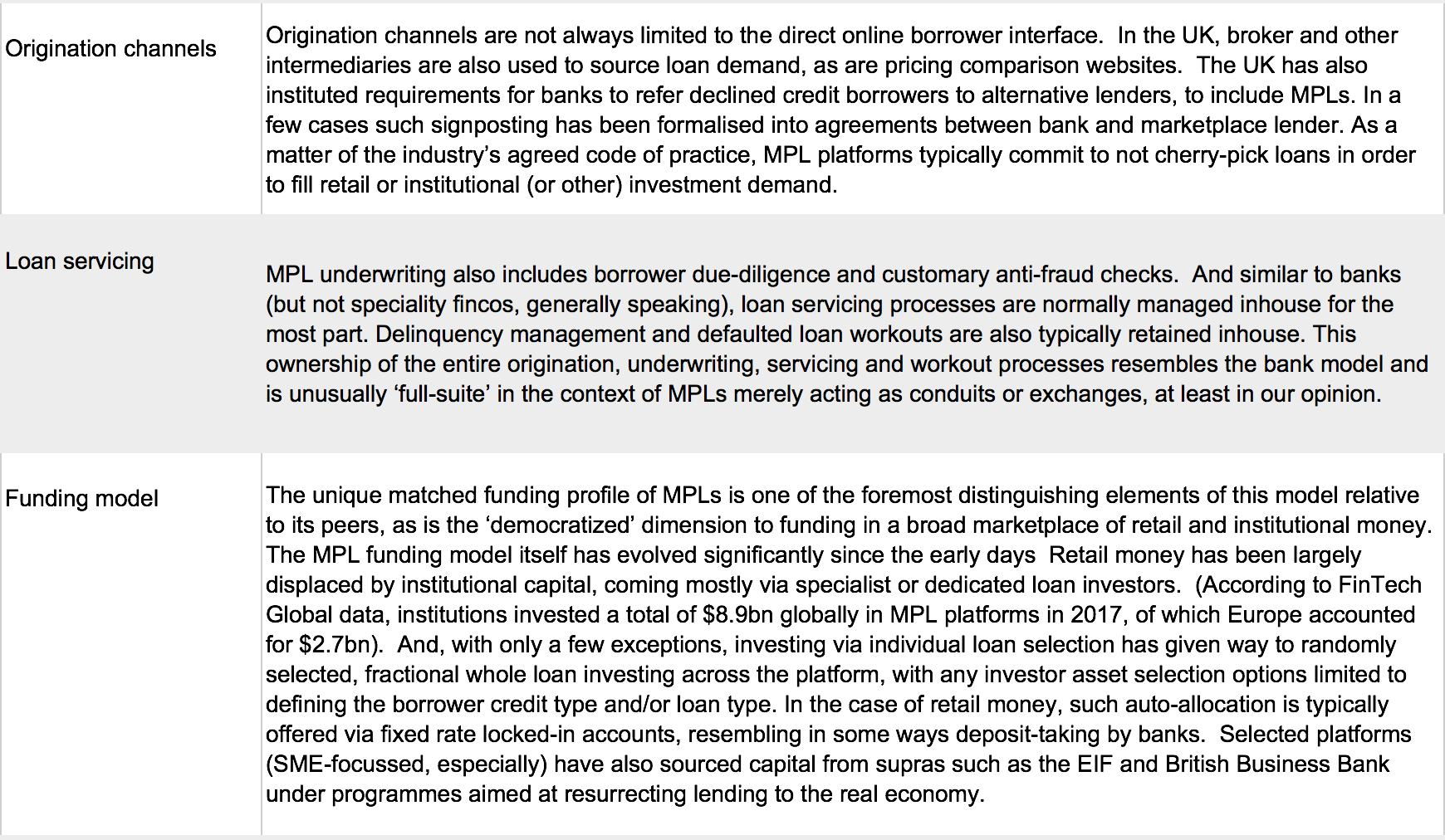

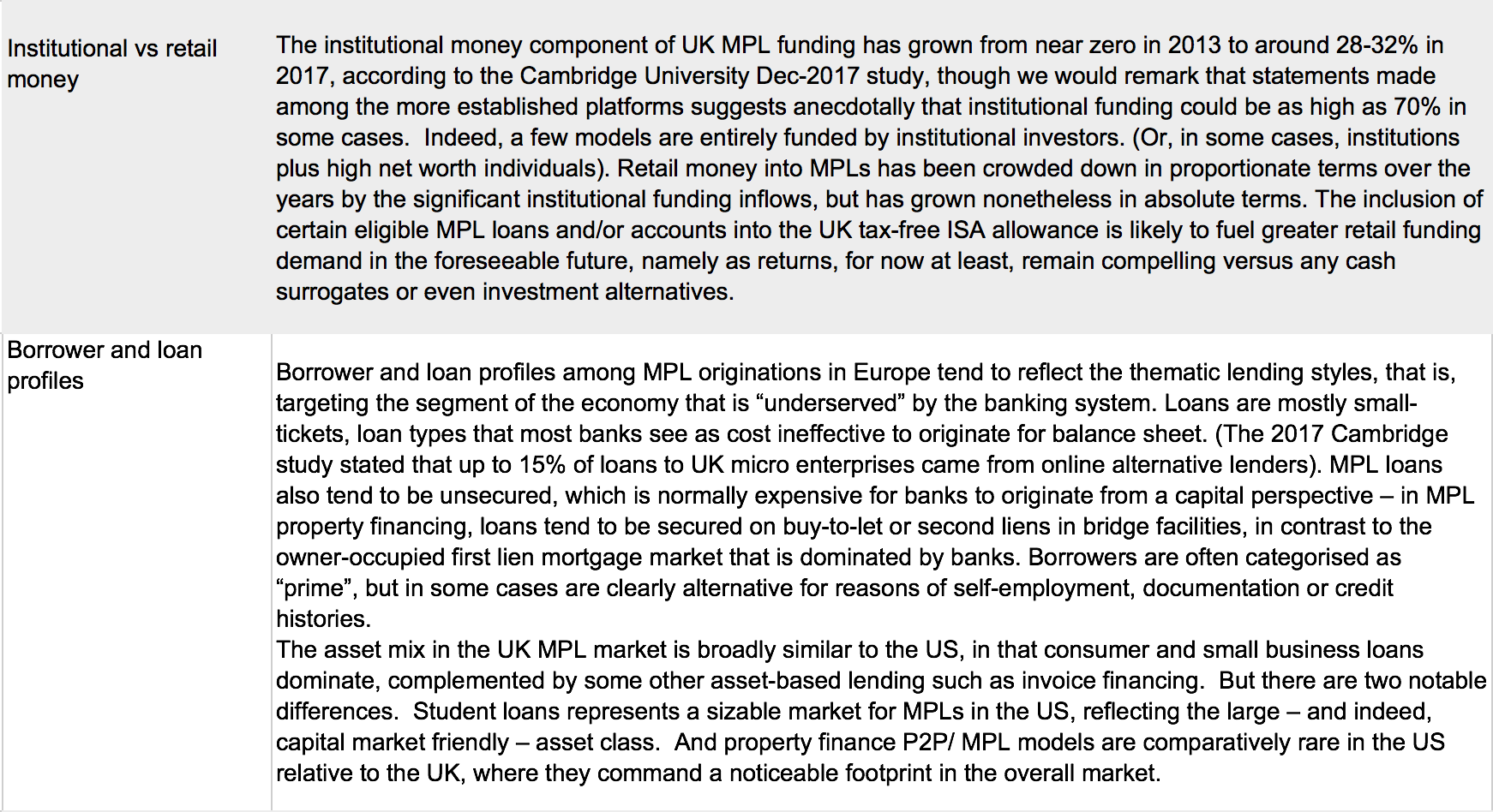

In this report, we look at the impact of the covid crisis on private and alternative credit markets in Europe, spanning mortgage, consumer and small-/ mid-cap corporate credit. On our estimates, this non-bank specialty lender-led market has a footprint of roughly €350bn in terms of loan stock, dominated by the UK.

The covid pandemic is of course an unparalleled crisis in its scale and intensity. And the policy-maker response has been equally without precedent, generally comprising a three-prong approach made up of exceptional monetary accommodation, emergency fiscal stimulus measures and loan forbearance initiatives. The response to the covid pandemic hitherto has already far surpassed policy actions taken during the 2008/9 crisis.

In the near-term at least, we feel the fiscal measures in place will provide appreciable support for debt servicing burdens while also cushioning any repayment shocks as some borrowers emerge from payment moratoriums. Household credit stands to benefit most in this respect, in our view. Rather than loan book credit deterioration, we see lender financing and/or liquidity distress as the main near-term casualty from the covid crisis, given the extent of forbearance on the one hand and the more selective liquidity within securitization and institutional funding markets on the other. (Non-banks and speciality credit assets generally fall outside central bank liquidity and asset purchase envelopes, with very few exceptions). This squeeze on many non-bank lender models may provide interesting private market ‘back-book’ opportunities in the coming months.

The longer-term crisis impact on private credit performance depends largely of course on its ultimate toll on employment and business survival. At this stage we see unsecured credit as being at most risk, save potentially for some higher margin loan books which may be insulated by adequately rich yields. Mid-cap corporate portfolios may also be vulnerable if default expectations in the larger-cap leveraged finance market is any guide. (Indeed, this crisis will be the first real test for private debt funds, and also for the likes of marketplace lenders). Residential mortgages should prove the most credit defensive, in our opinion.

Covid brings the 2010s alternative credit cycle to an abrupt end. In its aftermath, we see a fresh cycle of front-book opportunities re-emerging apace to coincide with renewed demand for specialty credit. Compelling risk-return economics (typical in any early-cycle lending) against the backdrop of prolonged ultra-low rates should underpin the merits of private loan book investing, once again.

Disclaimer

The information in this report is directed only at, and made available only to, persons who are deemed eligible counterparties, and/or professional or qualified institutional investors as defined by financial regulators including the Financial Conduct Authority. The material herein is not intended or suitable for retail clients.

The information and opinions contained in this report is to be used solely for informational purposes only, and should not be regarded as an offer, or a solicitation of an offer to buy or sell a security, financial instrument or service discussed herein.

Integer Advisors LLP provides regulated investment advice and arranges or brings about deals in investments and makes arrangements with a view to transactions in investments and as such is authorised and regulated by the Financial Conduct Authority (the FCA) to carry out regulated activity under the Financial Services and Markets Act 2000 (FSMA) as set out in in the Financial Services and Markets Act 2000 (Regulated Activities Order) 2001 (RAO).

This report is not intended to be nor should the contents be construed as a financial promotion giving rise to an inducement to engage in investment activity. Integer Advisors are not acting as a fiduciary or an adviser and neither we nor any of our data providers or affiliates make any warranties, expressed or implied, as to the accuracy, adequacy, quality or fitness of the information or data for a particular purpose or use. Past performance is not a guide to future performance or returns and no representation or warranty, express or implied, is made regarding future performance or the value of any investments. All recipients of this report agree to never hold Integer Advisors responsible or liable for damages or otherwise arising from any decisions made whatsoever based on information or views available, inferred or expressed in this report.

Please see also our Legal Notice, Terms of Use and Privacy Policy on www.integer-advisors.com

Read More

Update on Capital Relief Trades in Europe

Post by : admintegeradvisors | Post on : October 2, 2019 at 9:14 am

Steady Momentum Continues

Update on Capital Relief Trades in Europe (PDF Version)

Executive Summary

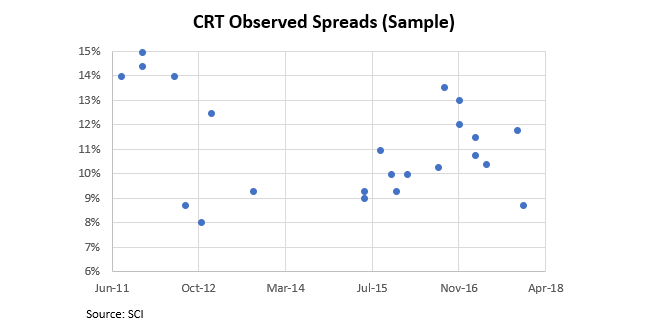

This article serves as an update to our original, in-depth report on credit risk transfer / capital relief trades (CRTs) published in the summer of 2018 (see here). Over the past year, primary supply of CRT tranches looks to have remained broadly range-bound, with the greater prominence of supras and development banks as protection buyers emerging as an interesting trend. Demand technicals have also remained stable, with the buyer base concentrated among the (still) few alternative credit funds that have long dominated as protection sellers, despite efforts at bringing in new investor types. CRT pricing has remained sticky, with the range of clearing spreads (8-12% typically) continuing to be enveloped – in our view – by the return thresholds of the buyer base on the one hand, and the implied cost of bank equity on the other. CRT pricing certainly looks dislocated relative to the superior historical credit performance of the asset class, as highlighted very recently in the EBA STS discussion paper which analyses the feasibility of an STS framework for synthetic (balance sheet) transactions. Returns of 8-12% for (historical) reference portfolio loss risks of less than 20bps underscores the compelling value in CRTs (after allowing for tranche leverage and any first-loss retention).

Regulatory developments have been more notable in the past year. CRTs fell under the Securitisation Regulation net from the beginning of 2019, being subject more specifically to the ESMA disclosure framework, compliance with which we feel is unlikely to prove seamless for CRT from a practical perspective. The extension of STS criteria to CRT, as recommended by EBA in the discussion paper (subject to additional criteria) is on the other hand a positive development for the sector. In our view, such endorsement could be (potentially) transformational ultimately, though any STS labelling is unlikely to have any immediate effects considering the current tendency for senior tranche retention and also an investor base that is generally unconstrained by regulatory capital considerations. CRT structures have seen few changes since a year ago, arguably the most noteworthy being the trend for thicker tranches (increasingly split into dual tranches for cost-optimization) as a means to achieving significant/commensurate risk transfer. The treatment of excess spread remains a key structuring consideration for protection buyers, with further regulatory guidance still forthcoming in this regard (the EBA discussion paper suggests exclusion of synthetic excess spread as a criterion for the STS label).

Going forward, we believe there remains a strong impetus for CRT issuance as bank equity remains precious, particularly with the CRR roll-out from next year and the full force of the Basel III capital framework taking effect in 2022. Maturity of the demand side is where we see the greatest potential upside for the CRT market, though we are cautious as to if/ when this might happen. Regulatory inclusion is arguably the most important factor in unlocking mainstream investor liquidity in the asset class, with better transparency also key, in our view. The US CRT market, which benefits from pricing and liquidity not dissimilar to highly commoditized spread products, is clear evidence of the upside that can come with greater liberalisation of the CRT buyside in Europe.

Market Technicals

Stable Primary Market Momentum

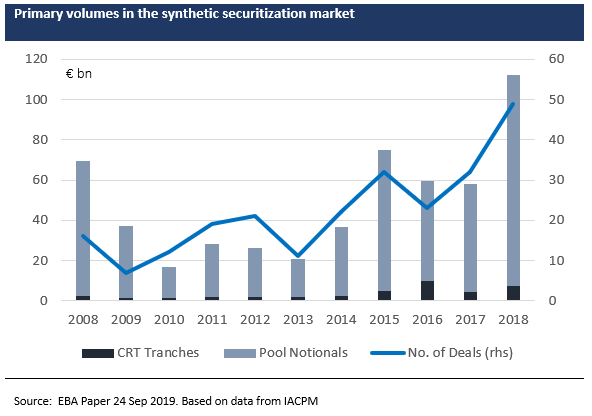

Since our last report on CRTs in mid-2018, the market as described by supply / demand technical has largely remained unchanged. Based on data from SCI, placed CRT tranches amounted to EUR 5.26 bn for the 12 months to July 2019, flat versus the EUR 5.48bn seen in the preceding 12-month period. Data released very recently in the EBA discussion paper (citing the IACPM data collection as the source) show broadly similar trends in terms of steady primary volumes measured by placed tranches although year-on-year some variations occur. We estimate reference pool notionals related to such European issuance at around EUR 69 bn versus EUR 80 bn in the preceding year, with the lower portfolio amount (but similar primary volumes) explained by thicker tranche sizes recently, as we outline below. Notably, the CRT deal count increased from 33 to 43 over the two 12-month periods, according to SCI data. Pool notional and deal count data from the recent EBA report (based separately on notifications by domestic regulators in Europe including the ECB) is again broadly consistent as far as we can see although again fluctuating year-on-year relative to IACPM or SCI data.

We repeat the important caveat that these figures are likely to somewhat understate the full extent of CRT activity in Europe. Private deal flow in the European CRT market, to include purely bilateral transactions, will not necessarily be captured by the data, yet make up a relatively significant portion of the market. Based on IACPM data recently published, which covers the entire synthetic securitization universe, only 18.6% of cumulative deal flow since 2008 until end 2018 was placed publicly (the remainder being private trades), with this ratio standing at 32% in 2018.

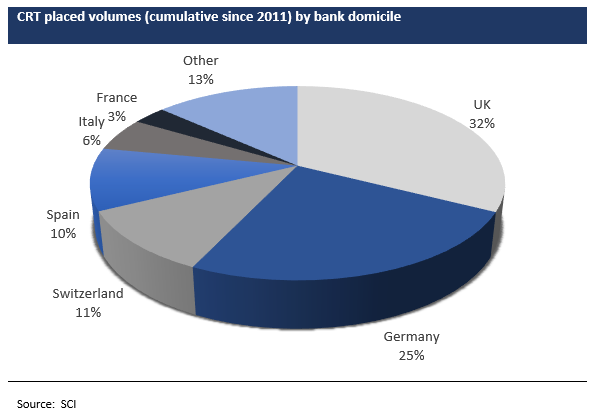

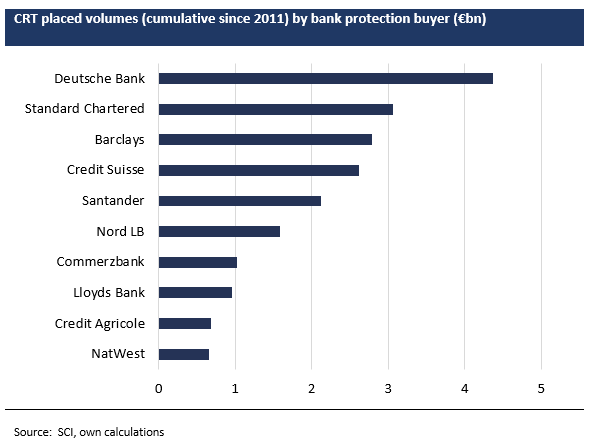

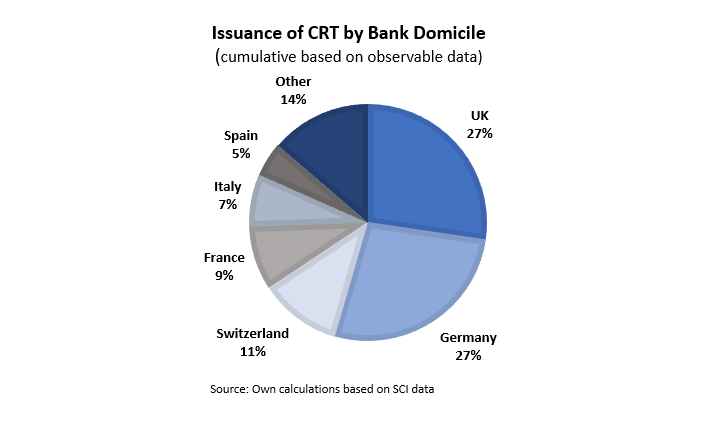

UK and German ‘SIFI’ banks continue to be the most active CRT issuers overall, but we note that Spain has seen a bigger market representation in the last 12 months, courtesy mostly of Santander. (We would add that the reference assets in this respect have been multi-jurisdictional). Interestingly, EIF/EIB-related transactions have featured more prominently in Italian and Spanish-sponsored deals as well as in some transactions from Central European institutions (namely Poland and Czech Republic).

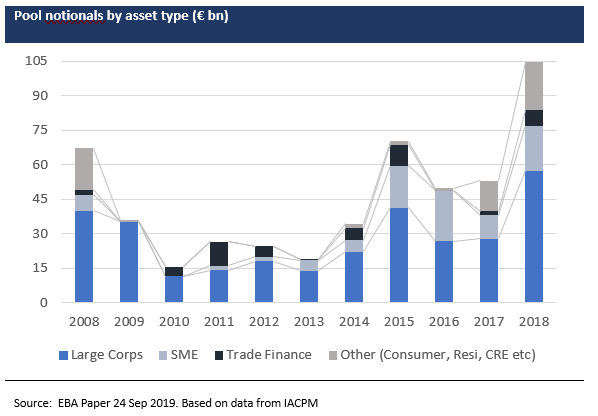

In terms of underlying portfolios, reference assets in Europe continue to be focussed on corporate and SME loans for the most part. However, this past year has witnessed an uptick in non-corporate reference portfolios, such as auto and consumer loans (via both tranched synthetic and full-stack true sale deals) plus selective residential and commercial real estate loans as well as project finance / infrastructure loan portfolios. As mentioned above, multi-jurisdictional portfolios are increasingly seen in the CRT market, indeed recent IACPM data points to the dominance of multi-jurisdictional risk transfer within the overall universe of synthetic securitizations (60%, to be precise), though our isolation of European bank CRT data suggest a more moderate share. As synthetic technology can efficiently facilitate the securitization of multi-country risk (certainly relative to cash securitizations), we expect to see more by way of such deals by European banks going forward.

Issuer Developments

Notable New Entrants

Large IRB banks continue to dominate the CRT market in Europe. Their market footprint has not materially changed over the last few years on our observations, reflecting the fact that these banks have the inherent advantage of having created efficient structures to fit their portfolio/ capital requirements as well as experience in engaging with their respective regulators. Experience with regulators is a key factor for successful CRT transactions in our opinion, given the absence for now of a prescriptive, rules-based regulatory framework for such deals (see section below). The in-house capabilities and infrastructure needed for CRT transactions can often be barriers-to-entry for new entrant banks in the CRT space.

The chart below shows the (observed) cumulative issuance volumes by bank domicile, highlighting the continued dominance of German and UK domiciled banks. As mentioned above, Santander has also been notable for ramping up their CRT activities in the past 12 months and we understand that French IRB banks have also become more active. But all things considered, the CRT issuer base remains somewhat concentrated relative to other capital market types. Any significant broadening of the issuer base would, in our view, require a conducive (and certain) regulatory framework, more transparency and better pricing ultimately for placed tranches, which in turn will necessitate further maturity and depth in the investor base.

EIF/EIB programmes continue to be important for the smaller and mid-sized banks tapping the CRT market, with such banks typically using the standardised approach. Reference assets in this case continues to be dominated by SME risk.

Arguably the most interesting development in the last 12 months was the embracing of CRT technology by a number of supranational and national promotional institutions. The Room-2-Run transaction from the African Development Bank was the first synthetic securitization by a multilateral development bank as a protection buyer freeing up capital. The deal involved a $1bn portfolio of 40 loans to financial institutions and project finance vehicles across Africa. Separately, the Dutch development agency FMO initiated a new program (‘Nasira’) whereby the agency can act as both protection buyer and protection seller, depending on risk motive. The novel program works with partner banks in developing markets such as Africa and the Middle East, ultimately enabling loan credit provision domestically to underserved SME market segments. We feel more such CRT activity from supras and promotional banks will be forthcoming, but recognise that much will depend on the extent of stakeholder support for, and endorsement of, capital relief trades.

The Investor Base

Evolving, Slowly

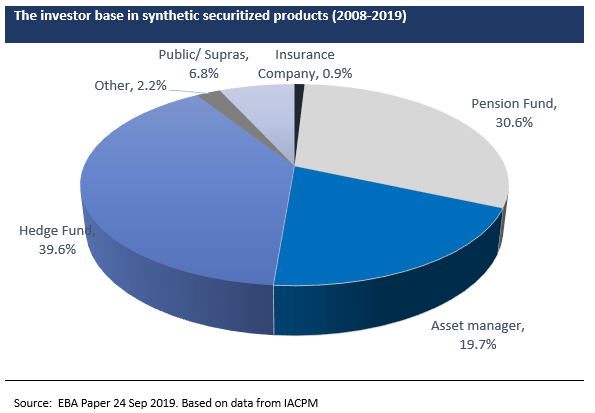

While there have been some new buy-side players coming into the CRT market over the past year, we would see the established incumbents – namely alternative credit/ hedge funds and a few pension funds – as continuing to make up the bulk of demand for the asset class. This intelligence is corroborated by the recently published IACPM findings, which also talked to the relative increase in the buy-side share of hedge funds in recent years, at the expense of pension funds.

Our own observations are that these established investors have generally increased AuM wallets dedicated to CRTs, allowing for bigger ticket purchases (EUR 100m+ sizes). This gives many such investors the ability to engage in bilateral deals, although we feel there are some issuers who still prefer syndicated (club) transactions given the potential benefits that come with such price discovery.

We also see ongoing efforts to bring more insurance companies into the market via unfunded formats, essentially as protection seller on the liability side rather than as investors in CRT tranches on the asset side. Such demand may be particularly relevant for upper mezzanine tranches, a relatively embryonic risk type that reflects the recent trend for split tranches in CRT deals (see discussion below). But to our knowledge there has been only one such confirmed transaction in the autumn 2018 referencing residential mortgages, where ING-Diba acted as the protection buyer and Arch Mortgage Insurance as protection seller. On a broader level, the recent IACPM data shows that insurance companies account for less than 1% of cumulative synthetic deal flow since 2008, albeit also pointing to an uptick in participation since 2017.

The potential demand from insurance money aside (both on the asset side as well as the liability side), it is not immediately clear in our view what the natural investor base for upper mezzanine tranches would be ultimately. Whereas we would expect some EIF activity for SME-related reference pools, the buyside for upper mezzanine risk in more traditional CRT types seems as yet uncertain in our opinion, not least considering that most of such tranches are non-rated at this stage.

Comparisons to the US CRT market

More CRT history in Europe, but still less mature

The US CRT market is younger, yet far larger than the European market if measured by deal flow. There are a number of interesting nuances, however.

The US CRT market benefits from a broader and deeper buyer base than for European CRT product, with such investors comprising mainstream money also, in contrast to Europe where alternative credit buyers dominate. But unlike Europe, the issuer base in the US is overwhelmingly dominated by the two mortgage agencies, Fannie Mae and Freddie Mac. Yet despite this issuer concentration, the US market is still much more liquid/ tradable than its European equivalent given that these two agencies have spearheaded a high level of standardisation and transparency across their CRT programmes, to include deep data on price and credit performance. By contrast, the European CRT market remains largely private and substantially non-traded.

To demonstrate the superior liquidity technicals in the US CRT market, we note that the Fannie Mae CAS program has seen cumulative issuance of $40bn as of July 2019, with secondary trading volumes of around $28bn in the last 12 months, over one times float of $27B. Liquidity, in turn, anchors the deeper buyer base, while also better facilitating repos and leverage-taking. For this and other reasons, the US CRT programs achieve significantly lower average protection costs relative to the European market.

Domestic investors remain the most important pocket of CRT buyers in the US. Fannie Mae has shifted to REMIC usage (Real Estate Mortgage Investment Conduit) in order further diversify their investor base. Recent initiatives suggest Fannie Mae is focussed on its programme appeal in Europe, stepping up their disclosure as a non-EU issuer in compliance with the new STS regulations covering EU investors. In doing so, Fannie launched a new website section specifically targeted at EU investors, thereby ‘exporting’ the practices of US CRT market transparency into Europe, where such disclosures are not yet visible with few exceptions.

The US CRT programs highlights clearly the potential long-term benefits to European bank CRT issuers from more programmatic issuance with bond market-style transparency and secondary liquidity support. But, for various (entrenched) reasons, we think more realistically that such maturity in the European CRT market is still some ways off.

Transaction Structures

Testing the product’s versatility

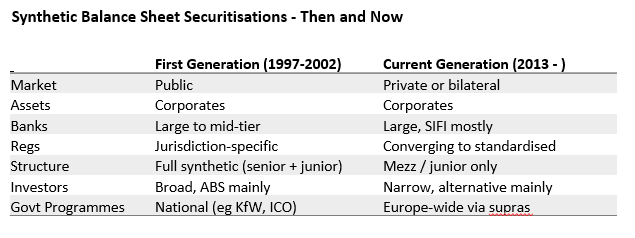

CRT transaction structures continue to be defined by regulatory considerations for the most part. In the absence as yet of any new regulatory framework that could shape (or re-shape) structural norms, there has generally been limited changes to deal structures since our report a year ago, save for a few notable developments as outlined below.

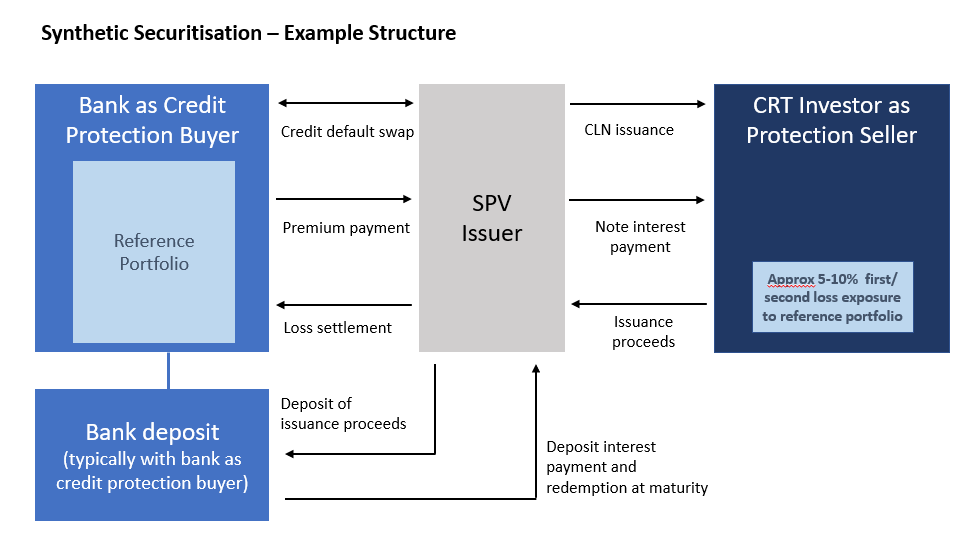

Most CRTs continue to be in synthetic format, however ‘full-stack’ true sale securitizations have become more prominent over the past year in the case of non-corporate reference assets such as auto and consumer portfolios. In such true sale deals, all tranches are normally sold subject to risk retention requirements (typically vertical with 5% retention of all tranches), though in some cases the senior notes are retained. The treatment of excess spread poses particular challenges in cash, full-stack securitizations, specifically because such income can be considered a securitization position from a regulatory perspective. Given the typically high excess spread in the likes of consumer or auto credit, the resulting capital consumption (in normal loss scenarios) can prove potentially prohibitive for the protection buyer, in that any capital relief from buying protection for the entire portfolio can be negated. While deal cash flow mechanics could possibly be tweaked so that any excess spread is extracted higher up the waterfall, we feel that there are no easy structural solutions that would comply with the spirit of the regulatory objectives in this respect. Our own view on this widely debated topic is that using a ‘gain-on-sale’ approach for future risky income that crystallizes such cash flow into a day-one securitized position held by the issuing bank (subject to capital requirements) may in some cases create disproportionate demands on capital relative to the capital position in a like-for-like unsecuritized portfolio.

In our opinion, the most significant structural development in the last 12 months has been the trend of greater tranche thickness among CRTs in order to achieve significant / commensurate risk transfer. Historically, based on our calculations, the average ratio of placed tranches to portfolio notionals in Europe was around 7%. More recently, we see this ratio frequently in the 10-11% area, which is notably different than the IACPM data for the global synthetic market (7.2% in 2018 vs 8.1% in 2017). Analysing what type of asset portfolios have been most impacted is challenging given the many different individual, transaction-specific parameters that also drive tranching. With thicker tranches generally, protection cost efficiency has clearly deteriorated for CRT issuers, mitigated to some extent by more dual tranche deals whereby an upper mezzanine tranche with lower clearing spreads is carved out. The development of thicker tranched CRTs is less noticeable among UK banks, however, reflecting the long-held PRA requirement for CRT tranches to be rated, which often necessitates thicker tranches than otherwise.

A key topical consideration in the CRT market is how to potentially synchronise CRT transactions with IFRS 9 accounting – that is, using capital relief technology to also deliver accounting benefits (release of loan provisions). The idea would be to reconcile credit event definitions more clinically with the IFRS 9 provisioning definitions, which to us amounts to a greater harmonisation of internal accounting and credit management policies. In practice many deals arguably already provide for IFRS Stage 3 loss coverage with the ‘failure to pay’ credit event typically capturing late-stage (90+ days) delinquencies, but efficiently (and economically) replicating coverage of Stage 2 provisioning poses greater challenges. Any release of accounting provisions would also depend of course on the attachment point of the most junior (placed) tranche.

The potential emergence of non-performing CRT transactions is also a topical market discussion. We are not particularly bullish on an NPL CRT market emerging in the foreseeable future, however, given fundamentally the challenges in fitting traditional credit event definition and loss settlement mechanisms into any defaulted asset pools with only recovery-based payoffs. Italian unlikely-to-pay loans (UTPs) would arguably be more compliant with traditional CRT technology, but being capitalised as already defaulted (which we understand is the typical CRR treatment) would kill the economics of buying protection. Above all, we believe that a significant impediment to any NPL CRT market development would be the lack of alternative investor appetite for this asset class, compared certainly to the depth of demand for cash, whole loan NPL portfolios.

Regulatory Considerations

Further notable developments and more to come

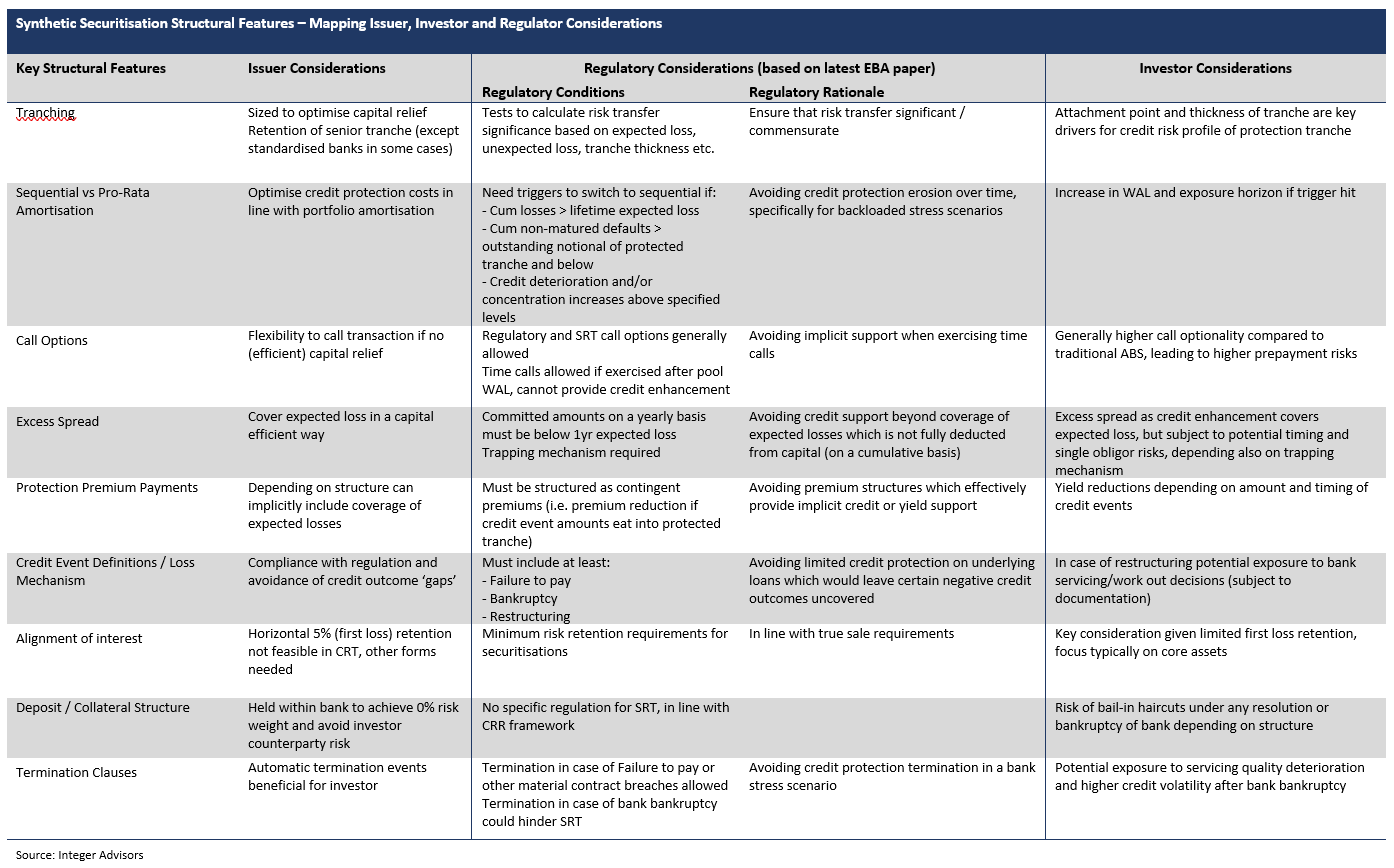

The key consideration for CRTs remains the regulatory landscape for such transactions. Regulatory capital relief remains the conditie sine qua non in the use of CRTs, aside from broader risk management objectives. In the absence of a defined and prescriptive regulatory framework for CRT usage, issuers are left to demonstrate significant / commensurate risk transfer to their respective regulators in order to achieve their capital relief aims. In this regard, the EBA 2017 discussion paper continues to be a de facto guide to structuring CRTs in addition to the CRR provisions.

Given that regulators will not ex ante sign off on CRT transactions, there is deal execution risks for potential protection buyers, a challenge that is especially significant for new market entrants without any precedence in engaging with their regulator around CRTs. Anecdotally we understand that there has been some convergence of regulatory application across Joint Supervisory Teams (“JSTs”) over the past year or so which is progress given some inconsistencies of the regulatory applications across EU regulators in the past (we would note that the UK PRA has overall still the most conservative approach).

Among the more notable regulatory-related developments over the past year that we would highlight include:-

- The potential emergence of STS criteria for synthetic transactions, based around the EBA’s consultation paper which was just published. This paper proposes a fit-for-purpose STS framework for synthetic deals that replicates the various criteria inherent in the main STS framework for cash securitizations, while taking into account synthetic-specific features related (mostly) to the protection mechanism, such as counterparty and collateral risks. The EBA paper raises the possibility of a ‘differentiated’ framework with potentially preferential terms for synthetic STS, although also acknowledges that any such preferential treatment would be inconsistent with the current Basel framework for synthetics. In our view, STS eligibility – while definitely welcome – is from an overall market perspective arguably less relevant for CRTs at this stage, in that transactions are ‘bottom-up’ whereby (largely unrated) junior tranches are sold to investors typically unconstrained by regulatory capital requirements. Moreover, senior CRT tranches are almost always retained in the current market, save for some deals involving banks using the standardised regulatory approach. In the case of the latter deals referencing SME assets, we would note that there is already STS treatment in effect for senior tranches under certain conditions as outlined in CRR Art. 270. All that said however, we recognize that STS eligibility would be a powerful de facto endorsement of the asset type, which should ultimately take the market out of the fringes and into the mainstream by both de-stigmatizing and standardising the product, in addition to more favourable capital treatment most relevant for the retained senior tranche. The STS discussion paper also highlights two important structural aspects: STS labelled transactions would not be allowed to have bankruptcy of the protection buyer (i.e. originator) as a termination event. Moreover, synthetic excess spread could not feature in an STS transaction. On the latter, we continue to believe that synthetic excess spread should be allowable to the extent that it would cover expected losses of the reference portfolio.

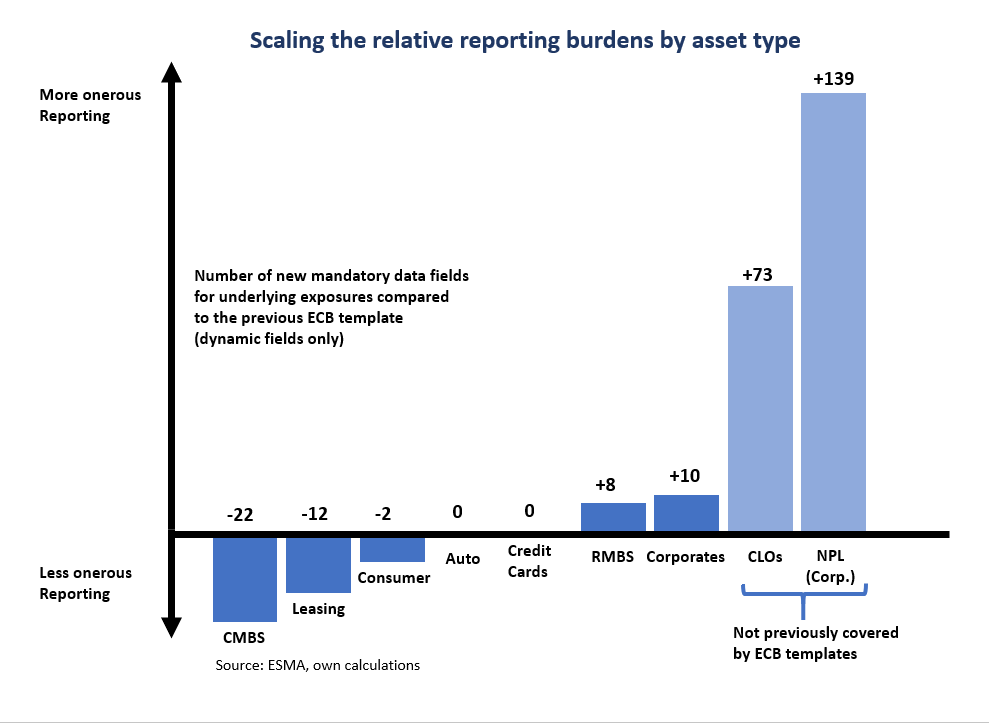

- The start of 2019 saw the implementation of the new disclosure regime (under the Securitisation Regulation) based on Art. 7 STS, the scope of which extends to private transactions. Most importantly, CRT deals have to follow the respective ESMA loan-level and (ongoing) investor report templates. This can be challenging in some areas given that the ESMA templates were essentially drafted for true-sale, cash securitizations and, as such, not all data fields can be seamlessly populated in the case of synthetic CRT deals. The ESMA templates do have a specific sub-section in the significant event report template for synthetic transactions (Annex 14), although this is not relevant for private

- The one key structural obstacle for efficient transactions remains the treatment of excess spread, both for true-sale and synthetic CRTs. We sense there is a consensus emerging to have a one-year (rather than cumulative) capital deduction if the synthetic excess spread is at or below the 1-year expected loss of the portfolio, based on an ‘use-or-lose’ approach (the recent EBA STS paper notwithstanding). For true-sale ‘full stack’ deals, any regulatory interpretation of (cumulative) excess spread as a securitization position can be a significant impediment to transaction economics, as discussed above.

Risk/Return Update

Recent data confirms historical credit (out)performance, underscoring value

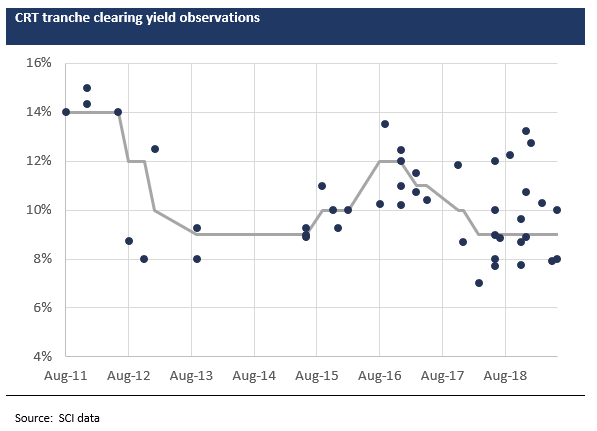

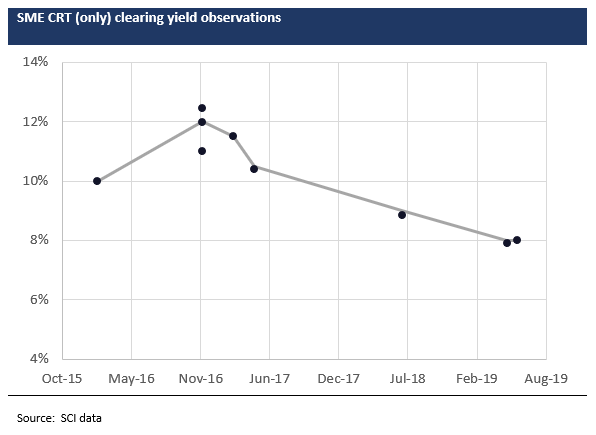

Large cap corporate and trade finance CRT yields (measured by primary market clearing coupons) have largely remained range-bound since our last report a year ago, albeit with a modest tightening seen in the range. On our observations, such CRT yields have trended between 8-12% in the past year, versus 9-12% in the preceding year. SME CRTs, by contrast, look to have tightened more perceptibly, typically pricing 1-2% inside of equivalent deals from 1-2 years ago.

Overall pricing behaviour continues to depend mainly on macro supply/ demand technicals – more specifically, as we had articulated last year, CRT pricing has remained enveloped by the return thresholds of the specialist investor base on the one hand, and the cost of bank equity on the other. The only meaningful exceptions to this otherwise range-bound pricing dynamic are deals where there is supra involvement (essentially EIF/EIB) as guarantor/ protection seller or investor in the capital structure. Both factors mentioned above – the narrow investor base and bank cost of equity – have remained largely unchanged over the past year, which in turn explains the stickiness of CRT yields. To be sure, liquidity in the CRT market still remains conspicuous for its absence, leaving few directional forces to allow spreads to break through their (long-held) resistance bounds. The lack of liquidity, or mainstream capital market sentiment more generally, has meant that CRTs remain an uncorrelated asset type versus public or tradable risk markets.

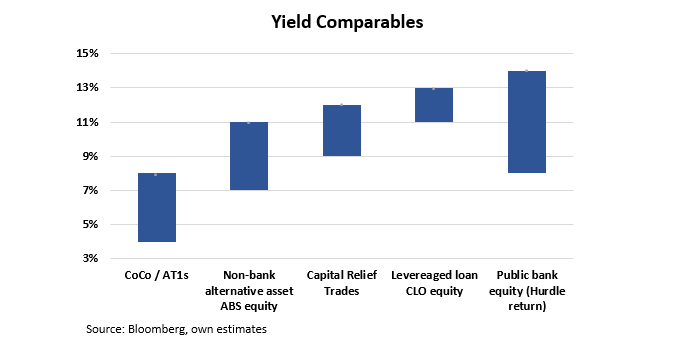

By almost any measure, CRT headline yields continue to look compelling versus most other comparable instruments, ignoring any justifiable liquidity premium. We would consider ‘comparable’ products as the likes of securitized residuals (including CLO equity) and bank AT1s or CoCos, which we discussed in some detail in our report a year ago. In the current market, as it was then, CRT yields remain generally superior to such comparables, except arguably for some CLO equity where returns may be indistinguishable from CRTs. We explore the relative value in more detail below.

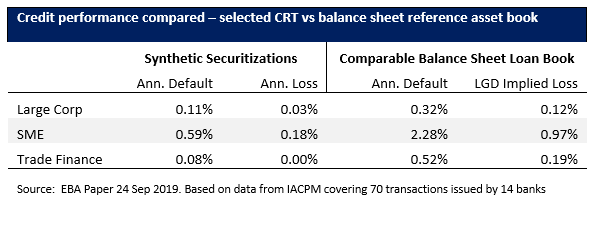

First, we feel its worth looking into the risk performance of CRTs, which the recent EBA paper is uniquely insightful courtesy of IACPM and rating agency data. (CRT loss performance data was generally unavailable before). Over the period from 2008 to 2018, the data shows that annualized default rates among large cap and SME reference portfolios amounted to only 0.11% and 0.59%, respectively. Write-offs annually stood at 0.03% and 0.18%, respectively. Such credit performance stands out versus most other comparable spread product. Indeed, the recent EBA report also highlighted rating migration data from S&P that shows the outperformance of synthetic versus cash securitizations since 2008. One key takeaway from the data provided by the EBA report is that the credit performance of synthetic reference pools has been consistently superior versus the same balance sheet (unsecuritized) assets of the institution – this suggests that there is an element of positive asset selection in the case of CRTs referencing core bank assets.

To provide slightly more balance to the bullish credit history described above, we would note that a few CRT deals were vulnerable to high profile UK-based corporate defaults over the past couple of years, to include Carillion, Interserve and selected others in the retail sector. We do not know the end-impact of such credit events at any deal-specific level, but these episodes are a reminder of the inherent portfolio risks among CRTs to idiosyncratic, single-name credit events in what can often be lumpy pools.

The above notwithstanding, richer-than-market CRT yields – in the context of its superior credit performance historically – underscores the compelling value in the asset class in our view, certainly for buy-and-hold money that can withstand illiquidity. Let’s compare with leveraged loan CLO equity, as a case in point. Nominal horizon returns on both CRTs and CLO equity is roughly in the same region, i.e., around 10-12% annually. Leverage, as measured by attach/ detach points, is also generally comparable. Yet CRTs have, historically at least, outperformed CLOs by an appreciable degree – since the 2008 crisis, CRT annualised default rates of 0.11% (large cap corporate reference assets) compares with leveraged loan annual default rates of 3.1% (Source: Fitch). The differences in default rates speak to the typically superior asset credit quality in CRTs versus CLOs, enhanced by likely positive credit selection in the case of CRTs. Moreover, the CRT coupon stream (protection premiums) is not vulnerable to lifetime portfolio cash flow risks, as in the case of CLO equity returns. CLO equity trades in a far deeper institutional market than any CRT product, however.

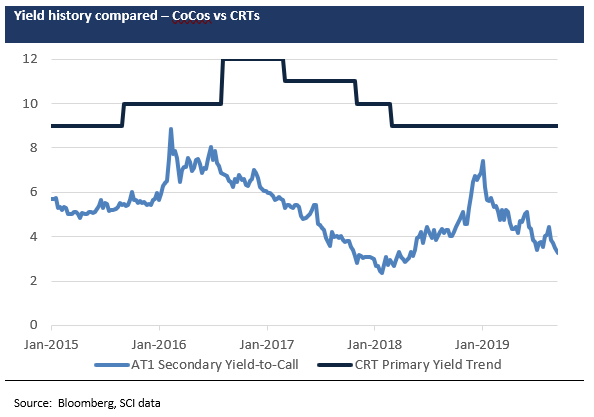

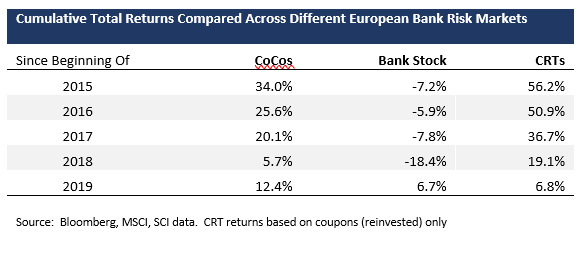

In our last report we discussed relative value considerations in comparing bank AT1s/ CoCos to CRTs, with the premise being the hybrid-equity parallels of both product types, notwithstanding some fundamental differences. CoCos have posted impressive cumulative total returns since 2015 (see table below), with yields-to-call currently (ca. 3-3.5%) re-approaching the historic tights seen in 2018. Yet CRTs can be shown to have outperformed based purely on coupon carry, at least using similarly discrete cumulative periods. The one exception is 2019YTD, during which reflation drove a sharp rally in high-beta spread products such as CoCos, whereas illiquid CRTs witnessed no similar correlated benefit. Our point here is that any outsized returns in non-traded, non-mainstream paper such as CRTs can only be fully realized over longer holding periods, with high coupon rolls making up for the anchored pricing.

Fundamentally, to recap our arguments from a year ago, CRTs provide for levered but narrow exposures to defined bank-originated asset credit risks (only), whereas AT1s/ CoCos (or bank stock, in the extreme) represent levered exposures to a broader mix of risks to further include operating, financial and event risks. Balance sheet credit deterioration (taken in isolation) has been far rarer a catalyst in triggering sell-offs in bank risk instruments over the recent past, relative to other risk factors. This arguably justifies the return outperformance of CRTs hitherto.

The potential for a better convergence of CRT pricing with its credit fundamentals remains very limited for now, at least in our view. For CRTs to trade like say CoCos, the market will need to be substantially “mainstreamed”, in terms of the buyer depth, dealer market-making, credit and price transparency and, not least, greater regulatory inclusion. Despite moving gradually in this direction, we do not feel that any such transformation will be seen in the short-term.

Disclaimer

The information in this report is directed only at, and made available only to, persons who are deemed eligible counterparties, and/or professional or qualified institutional investors as defined by financial regulators including the Financial Conduct Authority. The material herein is not intended or suitable for retail clients.

The information and opinions contained in this report is to be used solely for informational purposes only, and should not be regarded as an offer, or a solicitation of an offer to buy or sell a security, financial instrument or service discussed herein.

Integer Advisors LLP provides regulated investment advice and arranges or brings about deals in investments and makes arrangements with a view to transactions in investments and as such is authorised and regulated by the Financial Conduct Authority (the FCA) to carry out regulated activity under the Financial Services and Markets Act 2000 (FSMA) as set out in in the Financial Services and Markets Act 2000 (Regulated Activities Order) 2001 (RAO).

This report is not intended to be nor should the contents be construed as a financial promotion giving rise to an inducement to engage in investment activity. Integer Advisors are not acting as a fiduciary or an adviser and neither we nor any of our data providers or affiliates make any warranties, expressed or implied, as to the accuracy, adequacy, quality or fitness of the information or data for a particular purpose or use. Past performance is not a guide to future performance or returns and no representation or warranty, express or implied, is made regarding future performance or the value of any investments. All recipients of this report agree to never hold Integer Advisors responsible or liable for damages or otherwise arising from any decisions made whatsoever based on information or views available, inferred or expressed in this report.

Please see also our Legal Notice, Terms of Use and Privacy Policy on www.integer-advisors.com

Read More

Demystifying the UK Specialist Lending Markets

Post by : admintegeradvisors | Post on : June 4, 2019 at 2:00 pm

Private credit opportunities across consumer, mortgage and SME alternative loan markets

UK Specialist Lending Opptys_Integer Advisors 04 Jun 2019 (PDF Version)

UK Specialist Lending Opptys_Integer Advisors 04 Jun 2019 (PDF Version)

Executive summary

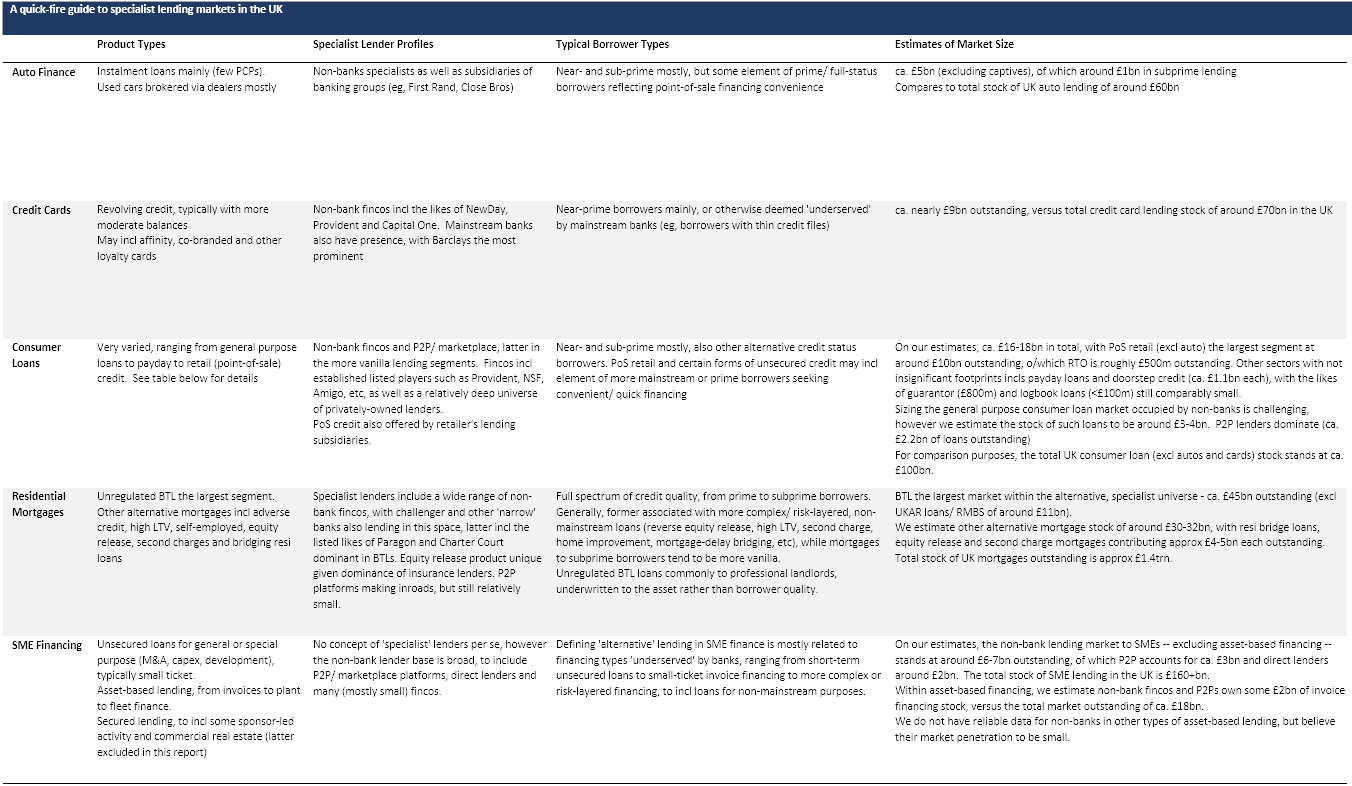

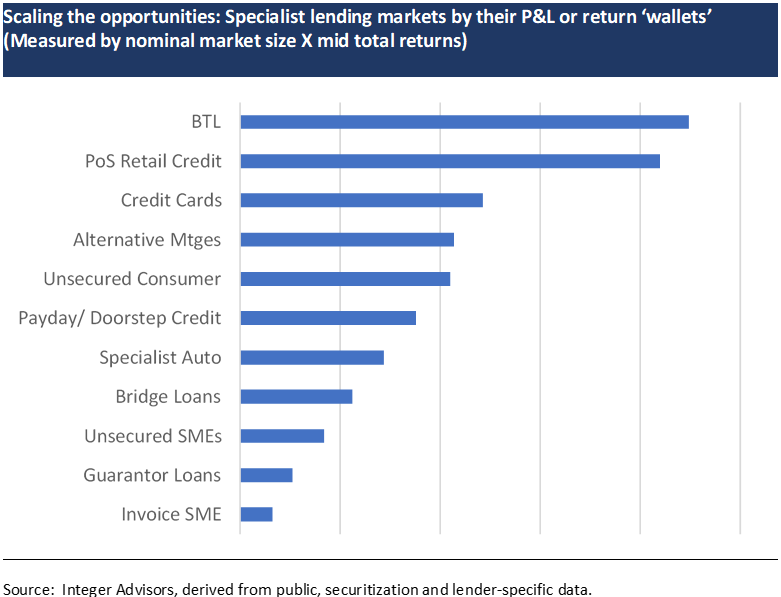

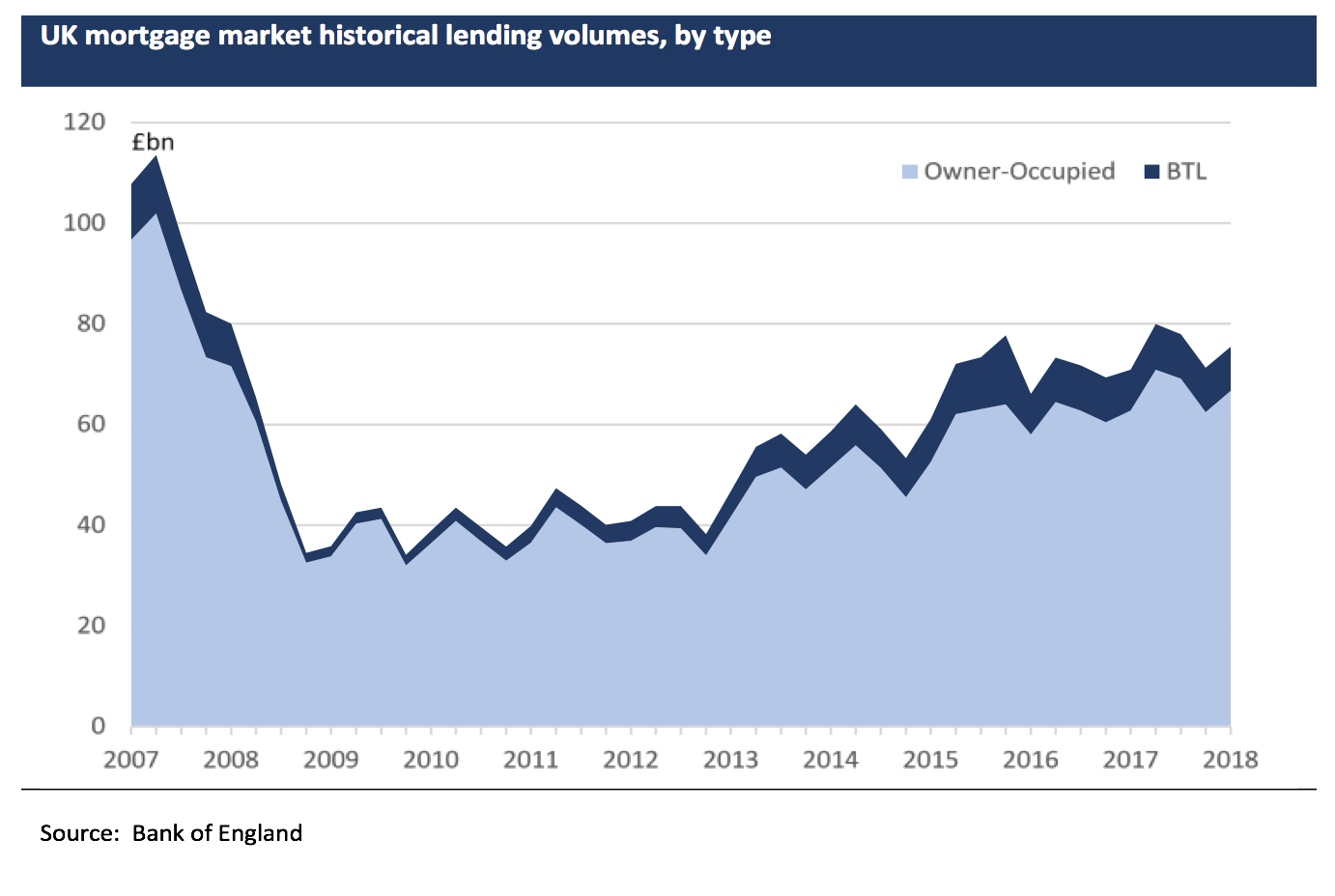

In this report we focus on investable opportunities in the UK specialist lending markets, across the consumer, mortgage and SME sectors. ‘Specialist’ lending can be generally defined as lending related to non-prime borrowers and/or non-conventional loan types, and by definition sits mostly outside of the mainstream banking system. The UK is distinct in being characterised by a relatively deep and diversified alternative loan market, unlike any other European credit economy. We estimate the size of this alternative lending market is around £100bn in terms of outstanding stock, or around 6-7% of the total loan market.

Recent growth of the UK specialist lending market stems equally from the post-crisis bank disintermediation opportunity as well as the sizable captive audience of “underserved” borrowers, which in turn reflects the relatively narrow lending remits of mainstream bank lenders. Looking across the lender, borrower and loan type continuum in this niche credit ecosystem, we would note the following: –

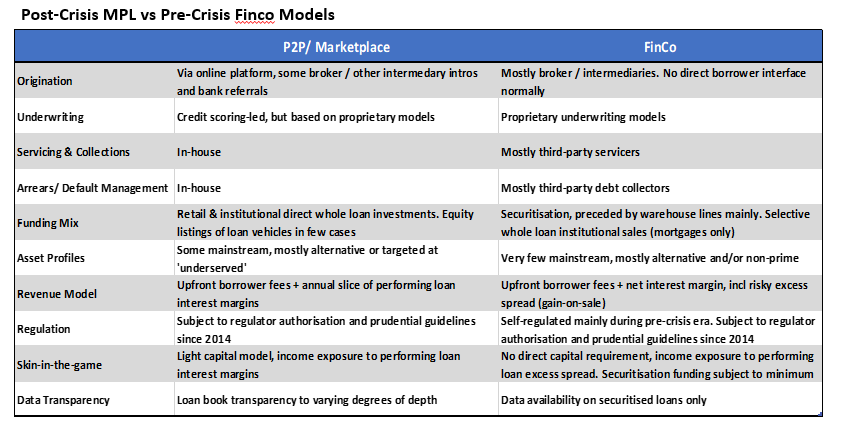

- Lenders are a mix of challenger banks typically with narrower lending styles, non-bank specialist fincos, P2P/ marketplace platforms and even institutional asset management-based direct lenders. Among the non-bank constituency, origination and servicing (including workouts) are sometimes outsourced. Many models – beyond P2P/ marketplace platforms – have also embraced digitization in recent years, in terms of the lending interface, underwriting and borrower relationship management

- Borrowers sourcing credit from specialist lenders are those with non-mainstream credit profiles. For the most part, such borrowers generally have thin/ no credit history, or are credit impaired / adverse given past uncured delinquencies, or are considered non-standard for other reasons (low income, self-employed, inconsistent address history, etc). Alternative borrowers can also include the highly indebted, whether household or small business

- Loans originated within the alternative space would typically be ‘off-the-run’, whether for reasons of complexity, risk-layering and/ or non-mainstream use of proceeds. In the SME market, specialist loans tend to be characterised by small ticket, unsecured credit.

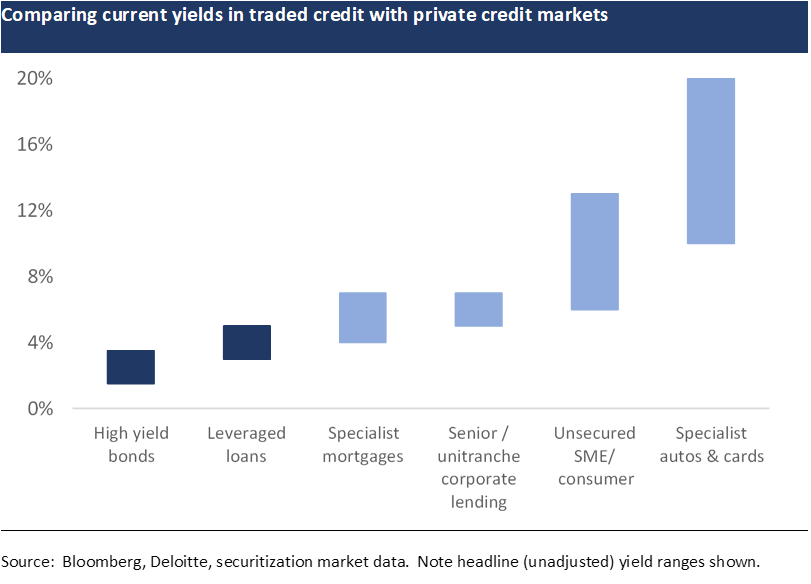

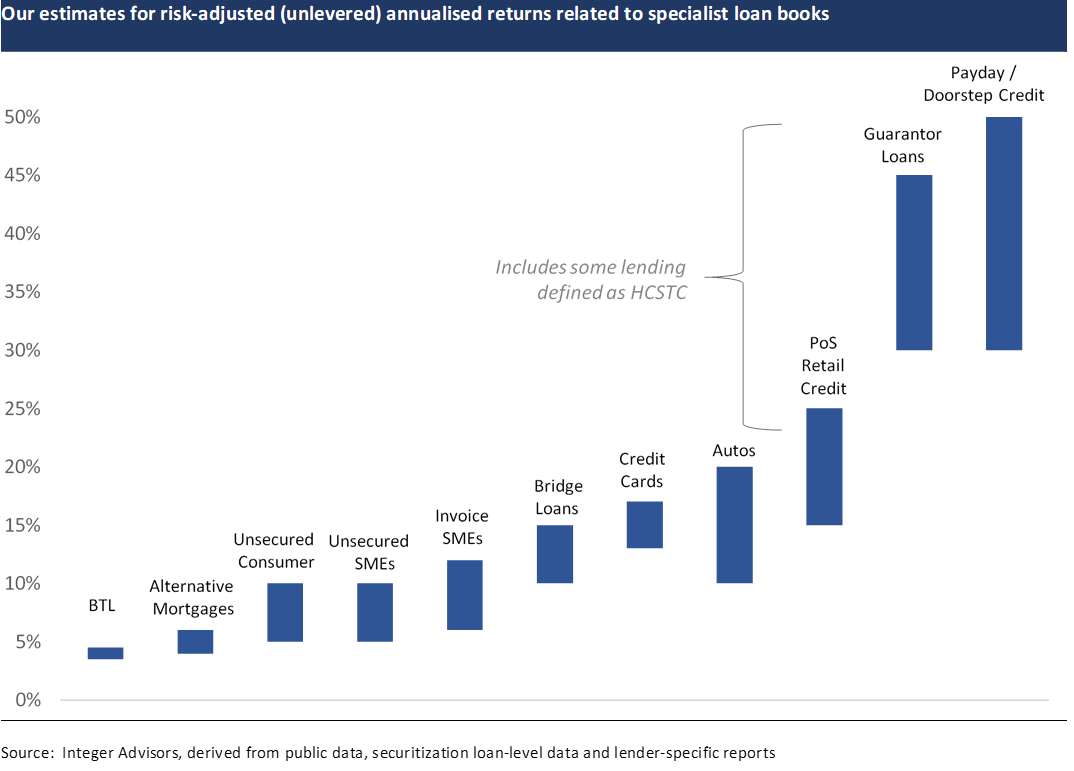

In scoping the potential private credit opportunities related to UK specialist lending, we use an approach that isolates such whole loan asset portfolios. Our analysis finds that unlevered loss-adjusted annualised total returns in these specialised lending opportunities can range from the 4-6% area in the most credit defensive end of the lending spectrum, namely specialist first charge mortgages, to ca. 10-15% in the more established consumer and SME lending markets such as autos, credit cards and unsecured loans, to returns in excess of 35% for very specialised, high cost consumer credit such as payday or doorstep loans. (In the case of the latter, we caveat the variability to such returns given potential loan loss / dilution volatility). We also find that selected sectors – such as residential bridge financing and guarantor loans – look undervalued versus their immediate peers given lending yields that seem rich relative to impairments experienced over the recent cycle.

Many loan types within the specialist lending space are inherently leverable. Such readily available gearing can provide enhanced returns for loan book (equity) owners, allowing even the most credit defensive lending types – which are typically the most leverable – to generate above-normal total returns. Leverage also of course provides the debt investment channel into specialist lending opportunities, whether via public securitized markets or private facilities (direct secured financing, future flow funding agreements, etc).

However, existing investable capital market opportunities related to UK specialist lending – whether listed lender stock, bonds or securitized products – do not seem to fully capture the loan book return economics outlined above, unsurprisingly given the liquidity premium implicit in such instruments, not least. (Certain risk assets – such as high yield or securitized bonds – look cheap versus traded comparables, however). Private market alternatives such as whole loans (via marketplace platforms) and managed loan funds appear better yielding in this regard. Among the latter, which tend to provide the most diversified exposure into specialist lending, we see the unlisted, PE-style fund opportunities as generally more compelling versus the listed fund (closed-end investment trust) equivalents. In theory at least, unconstrained funds should be the most nimble in being able to exploit these private markets across debt and equity opportunities.

Total returns from investing in specialist loan books (hypothetical as the case may be) look appreciably superior relative to ‘traditional’ forms of private credit, namely direct corporate lending. Moreover, there is little evidence that there has been any meaningful slippage in underwritten credit quality within the specialist lending markets, in contrast to direct corporate lending in which loan gearing and covenant protections have deteriorated in recent years, as widely documented. But on the flip side, private corporate debt – particularly in the large cap, sponsored space – is more readily accessible by institutional money, whereas specialist lending is of course harder to reach. For this reason, we think alpha generation among alternative credit funds invested in specialist lending markets has more to do with being able to originate these opportunities than it is just stock-picking

In our view, the key risks going forward, in terms of loan yield and origination resilience, comes from further regulatory reforms on the one hand, and lending competition on the other. Legislative changes can forcibly regulate loan margins and narrow the origination bandwidth via tighter lending standards, outcomes that already have precedence in the high-cost lending sectors. And what feels like the lack of competition in some segments of the industry today looks particularly susceptible to any reintermediation by mainstream banks, which could not only supress lending yields but also force specialist lending incumbents into more niche and/or riskier lending. (There are early signs of just such reintermediation in parts of the first charge mortgage markets, while bank online “flanker brands” are making inroads into other lending sectors). Credit performance over the longer-term horizon would likely be negatively influenced by any such drift into a riskier product mix, as it would of course under any fundamental deterioration in economic variables such as employment, disposable incomes or house prices. Notably however, unlike most other risk assets, we do not see specialist lending markets as being materially vulnerable to any normal shifts in interest rate paths going forward.

[All data used in this article – unless stated explicitly otherwise – is sourced variously from different public official sources including the FCA sector-specific reviews, securitization and P2P data, statutory reporting by listed lenders/ loan funds as well as other market research sources. Please contact us for more details and/ or further market insights derived from our data research]

Profile of the Alternative Lending Markets in the UK

Genesis of this niche lending system

Alternative lending in the UK has no precise or standardised definition that we know of, with the terms specialist lenders, alternative finance and underserved borrowers often used interchangeably in describing the full reach of lending activity within the sector. For purposes of this report, we look at lending that is characterised by non-prime borrowers and/or non-conventional loan types, outside of the banking system and mainstream loan markets. While this definition is by no means perfect, we believe it captures the bulk of activity in the alternative lending, and ultimately institutionally investable, space.

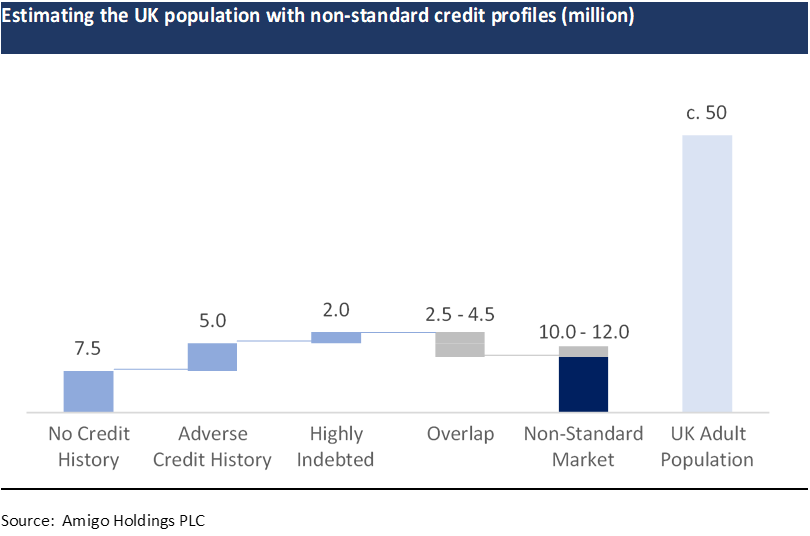

We estimate the size of this alternative lending market is around £100bn in terms of loan stock, with mortgages (unregulated buy-to-let products mainly) comprising the bulk of this footprint. On our estimates, this roughly equates to an alternative, or specialist, lending footprint of around 6-7% of total loan stock across the consumer, mortgage and SME markets. Various estimates put the likely population of ‘alternative’ borrowers – defined as having non-mainstream debt outstanding – at between 10-12 million people, or some 20% of the UK adult population.

The UK is distinct in being characterised by a relatively diverse range of loan types within the alternative credit space. Whether unregulated BTL or payday/ doorstep credit or alternative finance for small businesses, the UK alternative lending market is arguably the deepest and most mature among any in Europe, dating back some 30 years to the onset of financial sector liberalisation in the 1980s. Among developed economies, we feel only the US is characterised by a greater degree of specialist, non-bank lending.

Notwithstanding the established, decades-long momentum in the UK alternative lending industry, a number of key factors has served to reshape such markets over the post-crisis era, namely:-

- More onerous capital requirements and risk governance on established mainstream banks, which led to narrower and more regimented lending remits, in turn fuelling greater disintermediation opportunities for the likes of non-bank, alternative finance providers. Banks effectively pulled out of any ‘stretched’ lending into consumer and small business sectors, with such attrition compounded by the complete withdrawal by many foreign bank lending subsidiaries

- Reduced role of securitization as a capital market outlet, which not only proved destructive to many originate-to-distribute finco models in this space but also fuelled newer formats of ownership and funding among the private specialist lenders that survived the crisis. This gap was largely filled by alternative institutional investors – PE, for the most part – that have provided fresh equity and debt financing (whether via direct facilities or forward flow agreements, etc) to many specialist lenders

- Greater regulation across many aspects of this ecosystem, from lending and underwriting standards, borrower protection, capitalisation, securitization etc which has influenced everything from lending styles and target borrower markets to funding and capital considerations, not to mention the very survivability of a number of lending models. We expand on regulatory reforms later in this article.

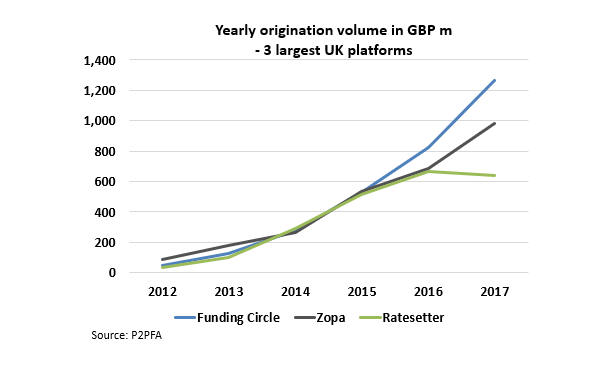

Lenders in the UK alternative lending space have historically been led by a constituency of finco originators simply called “specialist lenders”. Over the post-crisis era, such lenders have comprised larger, listed players as well as private fincos, often originate-to-distribute models seeded or funded by alternative/ PE investors, as mentioned above. Selected challenger banks with narrow, specialist lending styles have also emerged in the post-crisis period, as have online lenders such as P2P/ marketplace platforms, arguably one of the most notable developments in alternative finance in recent years. Institutional asset management-based direct lenders have also become more noticeable in the SME financing space than at any time in the past, though their lending activities tend still to be weighted more into larger corporate (often sponsored, leveraged) lending.

Save for the larger fincos and online platforms who enjoy direct borrower channels, most other speciality lenders originate loans via the established broker networks in the UK. (In the case of certain HCSTC markets, intermediaries called “lead generators” are also used to source product). Loan servicing and workout management are also commonly outsourced to third-parties, leaving many speciality lenders with funding and portfolio management responsibilities largely. Specialist lending has seen increased digitization in recent years, with online lending interfaces becoming very much the norm.

Borrowers in the specialist lending market are characterised typically by non-mainstream credit profiles. This could span thin or no credit history, credit impaired / adverse given past uncured delinquencies, or non-standard credit status for other reasons (low income, self-employed, inconsistent address history, etc). Alternative borrowers can also include the highly indebted, whether household or small business, and borrower seeking financing for non-mainstream purposes.

Loans originated within the alternative space are normally ‘off-the-run’ by nature, that is, products that are generally more complex and/ or risk-layered. We see a trade-off of sorts with borrower credit profiles in this respect, meaning that the more layered such loan products are, the more mainstream the borrower is likely to be. In other words, a subprime or credit-adverse borrower would likely only be eligible for a standard loan from an alternative lender, whereas a prime/ near-prime borrower could avail more complex products (high gearing, speculative loan purposes, etc).

Recent market growth and the impact of regulatory reforms

The market for alternative lending in the UK has experienced relatively steady growth overall in recent years, following the sharp contraction in the aftermath of the crisis. But growth has been uneven across the different sectors, indeed the overall observation masks somewhat divergent trends in individual markets. We would make the following notable observations: –

- Car finance in the alternative space experienced sharp growth up to 2016/17, prompting concern and greater oversight from macro prudential regulators. Growth has moderated more recently

- Unsecured personal loans – and especially point-of-sale retail credit – has also seen above-trend growth recently. By contrast, the likes of payday loans and doorstep credit – and indeed any lending that has come to be defined as ‘High Cost Short-Term Credit’ or HCSTC – have moderated in volumes, with greater regulatory oversight as well as better consumer credit literacy in recent years taking a toll on both lending and borrower demand

- Unregulated buy-to-let mortgages have also witnessed weakness in lending volumes in recent years since the sharp spike in the run-up to the new tax regime in early 2016, with macro factors and the fiscal disincentives weighing on the market more recently

- Alternative mortgage types such as residential bridge loans, second charge mortgages and equity release products have seen relatively strong growth in recent years, fuelled largely by household demand to realise value locked in home equity. Second charge loans have seen particularly strong growth recently, up 20% yoy in February 2019, according to EY

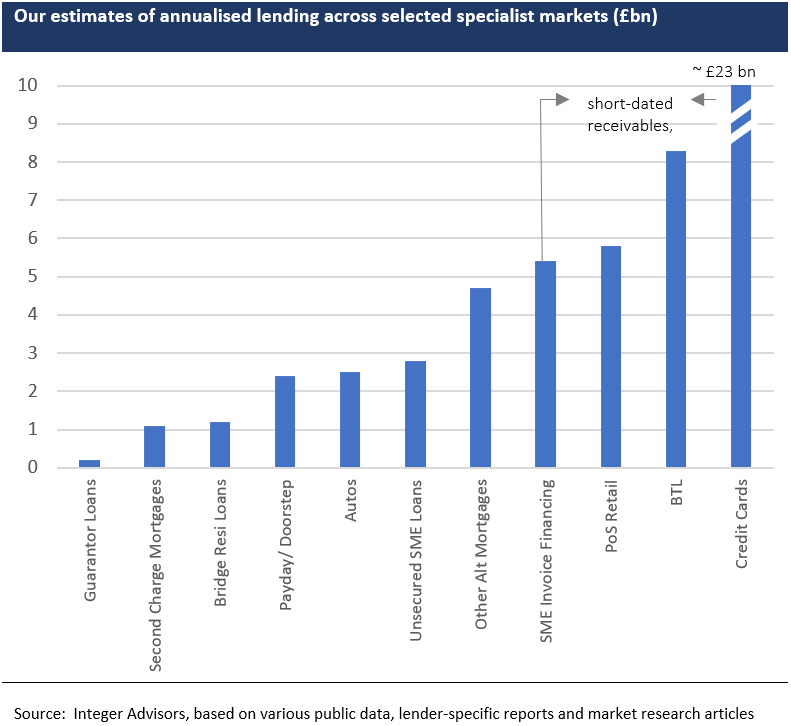

Growth in alternative SME financing looks to have been steady in recent years, however the availability of data (or even estimates) for this market is particularly challenging. From what we can tell, non-bank alternative lenders have noticeable footprints only in specialised markets such as invoice financing. In more vanilla (unsecured) lending where banks still dominate, the emerging role of P2P/ marketplace platforms in recent years has been notable, with such conduits accounting for nearly 10% of new SME lending flows (but still much lower in terms of the share of lending stock), on our estimates. Post-crisis rules requiring mainstream banks to refer declined SME credit to alternative lenders is a key driver of this emerging non-bank activity, in our view.

Regulatory reforms that have been rolled out in recent years are arguably the most significant factor shaping the market for alternative lending in the UK. Taken in its entirety, regulatory reforms in the post-crisis era have of course been wide ranging in their scope and aims, affecting lending activity across bank and non-bank/ alternative markets, to include mortgage, corporate and consumer lending. However, reforms to non-mainstream lending practices in the UK consumer credit market, in particular, have looked the most profound.

Consumer finance came under the regulatory net of the FCA from April 2014, prior to which the Office of Fair Trading was responsible for overseeing the compliance with the Consumer Credit Act, or CCA. The FCA supervision essentially covers all lenders and intermediaries, with the scope of regulations encompassing credit advertising, lending conduct and adequate transparency of loan terms (to include expressing lending rates as APRs) as well as debt management/ collection, among other practices. (The FCA rules, which reflect a principles-based regime, are enshrined in its Consumer Credit Sourcebook). Within the consumer finance space, credit agreements that are regulated are specifically lending to individuals (< £60,260) or sole traders/ micro partnerships (< £25,000).

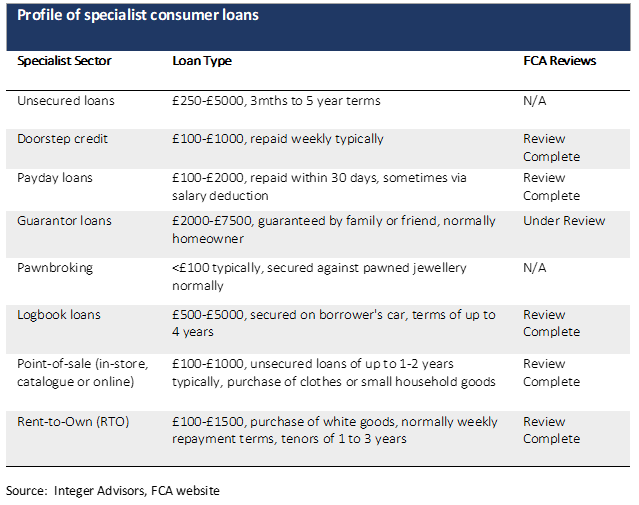

The most disruptive aspect of consumer finance regulatory reforms has been in the “HCSTC” sector, defined by the FCA as regulated unsecured loans less than one year in duration carrying interest at over 100% APR. Not all forms of HCSTC have come under greater regulation at this stage, only the likes of payday loans and certain types of RTOs. (Logbook loans – which falls under legislation governing Bills of Sales – as well as doorstep and catalogue credit are excluded from the rules, for now). The new regulatory regime for HCSTC, which came into effect at the beginning of 2015, is uniquely prescriptive. Aside from relatively comprehensive governance around responsible lending (including affordability checks) and product transparency, the new rules also feature economic limits on lending, namely:-

- Cap on interest rates (including fees) of 0.8% per day (nearly 300%+ on simple annualised basis). Further, default fees are limited to £15 per loan

- Overall total borrower costs (interest + fees) capped at 100% of sum borrowed

- Limits to loan rollovers of two times, with similar limits for lenders seeking continuous payment authority

- And in the case of RTO loans, new rules since April 2019 regulate pricing of ‘bundled’ goods sales (where the bundle includes insurance, warranties, etc), in effect capping the cost of the non-goods element at the cost of the goods themselves. Additionally, firms are required to conduct price benchmarking exercises to mitigate risks of overly inflating goods prices, often for reasons of subsidising credit costs.

The reforms have had far-reaching effects on the industry, not least on the scope of originations and lender profitability. (According to a CMA report, payday lender returns on capital were as high as 40+% in 2013 on the eve of the new regulations, falling sharply since then). Aside from shrinking the lender industry, the new regulations have also de facto shaped typical loan structures in the marketplace, in terms of rates, tenors and the amounts lent, as lenders have attempted to limit the regulatory impact or bypass the new rules altogether. However, the flip side of reduced lender profitability has been better default behaviour, according to anecdotal evidence. We see the reforms as also helping to cement the longer-term viability of certain forms of specialist lending, albeit at the likely expense of origination opportunities.

Dissecting Returns in the UK Alternative Lending Market

In this section, we analyse hypothetical total returns that can be derived from such alternative loan types, ahead of discussing current investable opportunities in these markets. We use an approach that isolates the whole loan asset portfolios. By this we mean looking at nominal yield and loss estimates related to typical loan books which are hypothetically carved out of the lender, in effect therefore net (or loss adjusted) portfolio income margins, which are of course distinguishable from opco equity returns. Where possible, we also adjust for any ancillary fee income that supplements loan book yields as well as operational costs related to loan portfolios (servicing and delinquency management mostly), with such cost estimates derived mostly from securitization transactions.

Sizing potential risk-adjusted loan book returns

On a wider observation, we would note that nominal loan book yields in specialist/ alternative lending markets in the UK are generally higher than the equivalent in most of developed Europe (currency unadjusted), and certainly versus the core EU credit economies, which remain heavily banked by comparison. However, relative to like-for-like alternative loan products in the US, lending yields look much less distinguishable, indeed in certain sectors (subprime consumer finance, for example), nominal loan yields in the US appear richer, unadjusted however for risks or the currency basis.

As we elaborate below, yields in the alternative lending space range from ca. 4-6% among the most defensive loan products (mortgages namely) to upwards of 100+% for very specialised, high cost consumer credit. Yields on most specialist loans and mortgages have been largely range-bound in the past few years. Notable exceptions however are the likes of payday loans, in which both lending rates as well as fees have been driven lower by the HCSTC regulatory reforms from 2015, not to mention pressure from consumer groups. Near-prime credit cards also stand out given portfolio yields that appear very sticky, having been mostly unchanged since the pre-crisis days. Our take on loss estimates over the past year or two in specialist sectors – sourced variously from FCA reviews, securitization and P2P data as well as statutory reporting by listed lenders/ loan funds – also highlights clear demarcations by lending types, which roughly mirrors loan yields

Coming now to total risk-adjusted returns related to (hypothetical) investments into such loan books. Total unlevered returns after losses tend to cluster into the three bands, in our view, described by their headline yield ranges and estimated loss experiences: –

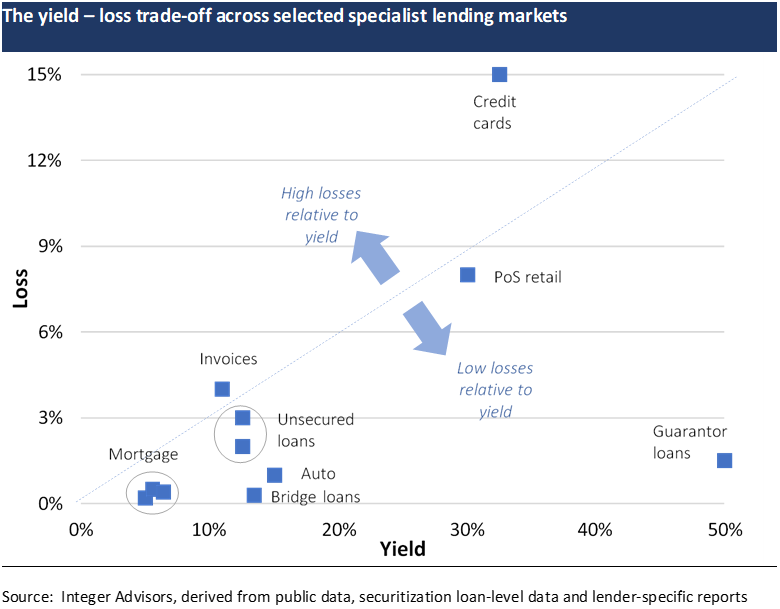

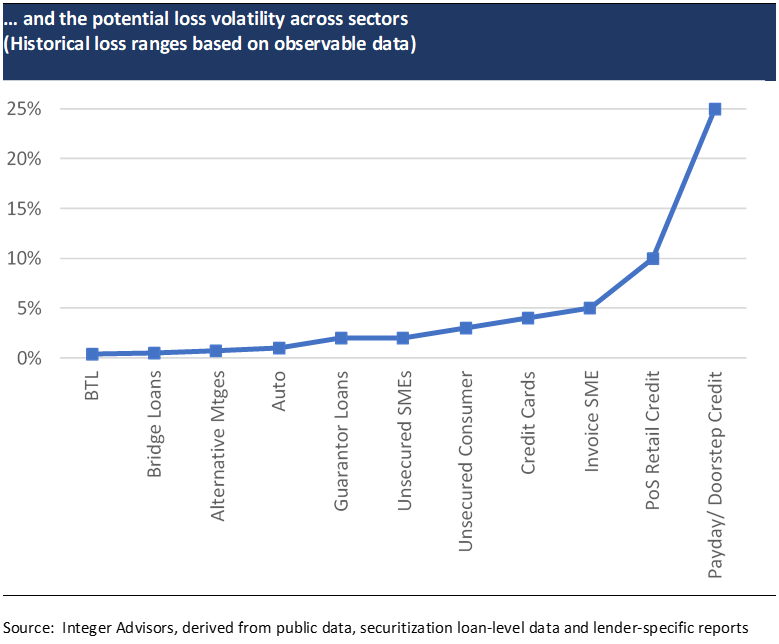

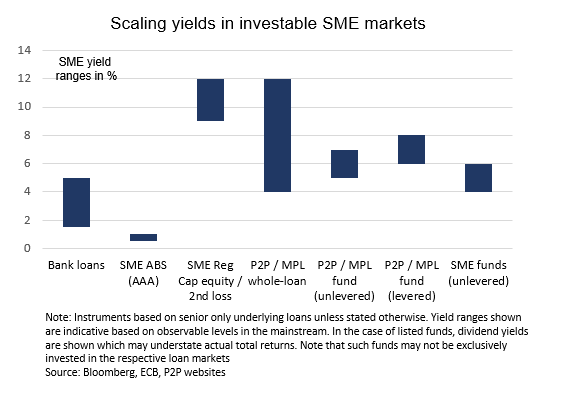

- Starting with the most credit defensive end of the lending spectrum, investing in specialist mortgages – comprised of unregulated BTLs and other alternative products (adverse credit, high LTV, etc) – looks to generate total returns in the 4-6% range, with higher quality BTLs in the lower end of that range and the likes of second charge products at the upper end. Residential bridge loans are an outlier by most return measures, as we touch upon below. First charge mortgages typically yield between 4.5% and 6% including fees. Second charge mortgages usually yield 6.5% or higher, depending on risk profile. (All of these observations are corroborated by respective RMBS pool yields). Total returns are not far off such yields given the superior credit performance of mortgage products, where annual realised losses are typically no more than 0.4%. There has been little loss variability among mortgages over recent cycles. Residential bridge financing is a notable outlier, however. Lending rates of between 12-15% typically have little incremental losses, relative to other owner-occupier or BTL mortgage products, to show for it. Low losses in bridge loans are explained by the typically conservative LTVs among such products, averaging only 55% in 2018, according to MT Finance (and up from 45% a couple of years earlier). Bridge loans are also an outlier from a tenor perspective, being far shorter dated (< 18 months typically) than other mortgage types, which normally have weighted average lives of anywhere between 2 and 5 years, notwithstanding final maturities that can be up to 25 years. Second charge mortgages seem also to be somewhat undervalued by this same measure, albeit to a lesser degree

- Total unlevered investment returns in the bulk of established consumer and SME lending – such as autos, credit cards, unsecured loans, more vanilla point-of-sale credit and invoice financing – look to be in the high single digits to say around 15%. Better quality unsecured loans to households and small businesses tend to generate risk-adjusted returns in the high single digits, whereas the likes of near-prime auto and credit card lending fall in the 10-15% range, generally speaking. Durations for such assets range from the ultra-short, revolving types (cards, invoices) to term loans typically up to 2 or 3 years in maturity. The above findings are based on headline lending rates that fall mainly in the 10-20% range, with many such ‘mid-cost’ specialist loans originated by a wide spectrum of lender types, including P2P platforms. Near-prime credit cards stand out for their appreciably greater portfolio yields in in the 25-40% range, however such portfolios tend to exhibit higher charge-offs as well, typically in the 14-16% area. The more vanilla forms of unsecured consumer and SME financing can be shown to experience losses in the range of around 1-4%, with auto financing typically in the lower end of this range (subprime loans excepted).

- And finally there are the highly specialised consumer finance markets that are priced at 50+% yields (and often greater than 100% or even 200% annually). Such loan types include payday, RTO, doorstep credit, logbook and guarantor loans, many (not coincidentally) falling under the auspices of HCSTC as defined by the regulator. For the most part, borrowers in these loan categories are subprime (or ‘deeply’ adverse in some cases) in terms of credit scoring, rather than having non-standard credit statuses for reasons other than payment behaviour, as is sometimes the case of borrowers in other specialist lending markets. Loans in this category tend to be short-dated but can extend up to 3 years in tenor. Indeed, regulatory reforms put in place since 2015 have, by all accounts, fuelled a lengthening of loan terms as lenders seek to minimise the impact from the rules. In this higher-beta end of the market for specialist consumer loans, losses tend to vary relatively significantly – from around 5% of annual write-offs in the case of certain RTOs to nearer 10% for logbook loans and higher risk PoS financing to 40%+ for the likes of some payday and doorstep credit, in which of course lending rates are typically in the 100%+ area. Volatility around these ranges varies noticeably given what can be highly unpredictable credit exposures. Loss-adjusted total returns in such specialist consumer loans can (hypothetically) be in the 35%+ range, however as remarked above there is noticeable variability to such returns given loss variations as well as servicing costs, which may not be insignificant in such loan markets. Our observations are therefore academic for the most part. Moreover, the very small market footprints for some of these high cost credit sectors would arguably make them almost uninvestable for all intents and purposes, from the standpoint of institutional money. Yet, there are some interesting observations to make. Segments such as guarantor loans and certain RTOs, for instance, can be shown to exhibit impairment rates that are appreciably better than the broader sector, yet are based on lending rates that largely mirror the market (40/50%+ annually). The potential volatility around such losses notwithstanding, there is evidence to suggest that credit performance among such highly specialised lending sectors is much more uneven than otherwise indicated by the very high loan yield ranges.

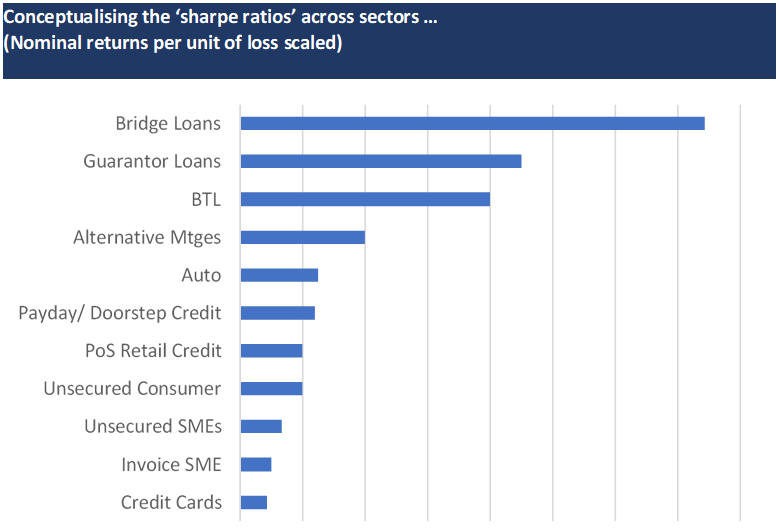

The linear relationship between loan yields and expected losses is evident to some extent in the specialist lending markets, but as highlighted above, by no means is this correlation universal. Sectors such as residential bridge financing and guarantor loans look ‘undervalued’ against immediate peers, precisely given lending yields that look rich relative to low and predictable impairment risks over cycles.

An important caveat to our discussion above is the potential variability of underwritten credit risk and loan margins within any one specialist lending sector. While we feel the above analysis captures the bulk of loan profiles (or the ‘bell’ of normally distributed observations), loan credit quality and yields can vary – sometimes significantly – in any given sector, largely reflecting the different lender models and risk appetites. Take auto finance for instance. Subprime auto lending is characterised by markedly different risk/ return metrics than near-prime or other alternative auto loans, as highlighted in the recent FCA review of the sector. Loan rates of up to 40% are not uncommon in auto finance originated to adverse credit borrowers, but this only makes up an estimated 3% of total auto lending, according to the FCA. Conversely, not all specialist consumer loan markets such as payday lending or catalogue credit are priced at very high rates – there is equally a ‘tail’ of the market that caters to better quality borrowers (often seeking financing convenience instead of rate shopping), which carries yields that are more normalised. We would also highlight that specialist mortgage markets have very thin ‘tails’ in this respect (that is, there is very little outlying lending styles described by meaningfully higher loan risk/ yields), arguably given the widespread rules around underwriting standards based on affordability prescriptions.

The role of leverage in investment returns

The use of gearing in private loan markets is common, with opportunities in UK alternative lending no exception. Indeed, many asset types within specialist lending are inherently leverable, particularly of course the stable, fixed income-like loans, such as mortgages.

Leverage allows loan book (equity) owners to enhance returns. Such equity investments are typically represented – to varying extents – in managed loan funds, whether listed trusts or private unlisted PE-styled funds. Our proceeding discussion looks at hypothetical leveraged equity returns across different loan types, and is conceptual rather than scientific given that we are using a very broad-brush approach with one-size-fits-all assumptions. All we are doing is demonstrating that returns can be appreciably enhanced through leverage, adjusting the extent of gearing allowable by asset type so as to make the end-findings comparable.

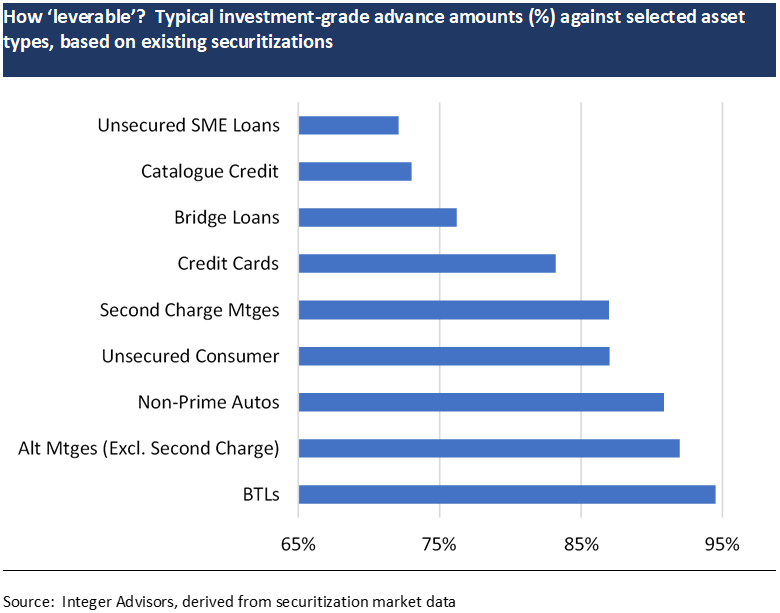

In order to size the potential gearing quantum by asset type, we consider risk-constrained leverage – in this case we define the latter by the typical attachment points for investment-grade financing advances against each loan book type, which we derive from existing securitizations. (By definition therefore, gearing thresholds here are dependent on rating models for the respective asset types, which in turn will be influenced by a host of factors including credit resilience and performance track records, among many others). Our findings show – unsurprisingly – that the more credit defensive (or predictable) and established sectors, such as mortgages and autos, are generally more ‘lever-able’ versus the likes of unsecured SME or consumer credit. Assets such as BTLs or alternative first-lien mortgages, or indeed granular specialist auto loan pools, can be geared (using investment grade facilities) 10-15x, whereas the equivalent risk-constrained leverage ceiling for bridge loans or unsecured credit or specialist high cost consumer lending seems to be nearer 3-7x. Near-prime credit cards also fall in the latter category.

With such leverage, established sectors such as specialist auto loans look to generate among the most compelling total returns for equity positions in such loan books, notwithstanding the academic exercise herein. Even sectors such as BTLs can (hypothetically) generate equity returns into the 30%+ range with conservative extents of gearing. Our point here is that looking at risk-adjusted unlevered returns alone does not capture the full investment case. By exploiting leverage, total return differentials for equity between the more established markets and the high-beta specialised lending sectors (such as say payday or doorstep credit) look much less distinguishable. Employing leverage is not without risks of course, in effect gearing in this case involves taking incremental financial risk to get closer to high cost, high (credit) risk lending returns.

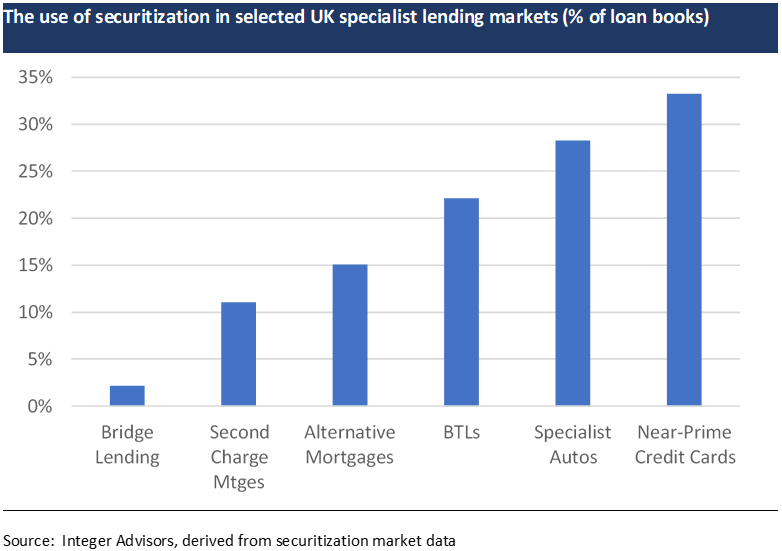

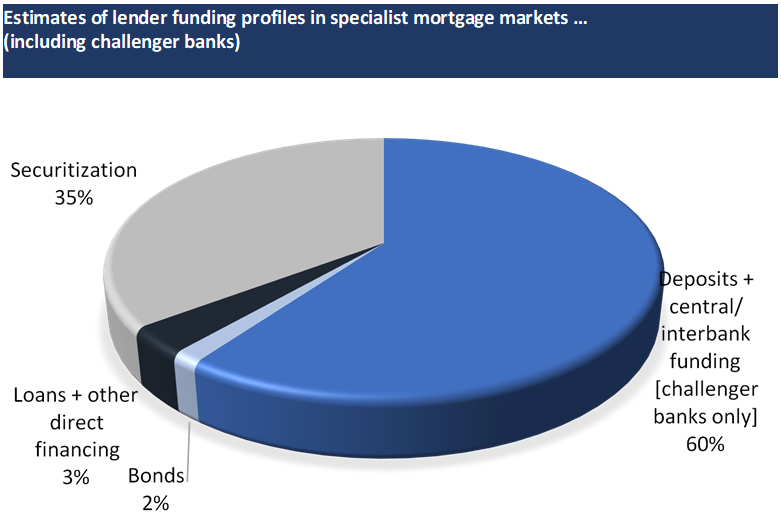

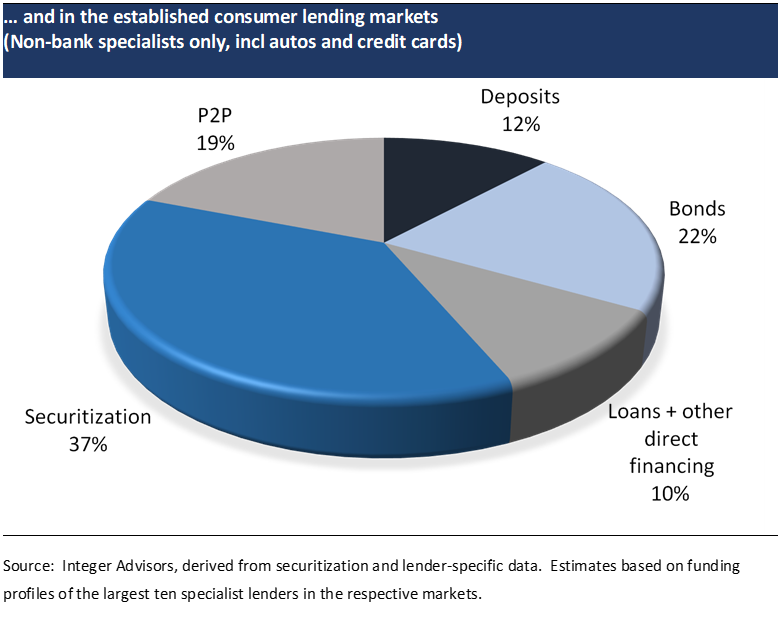

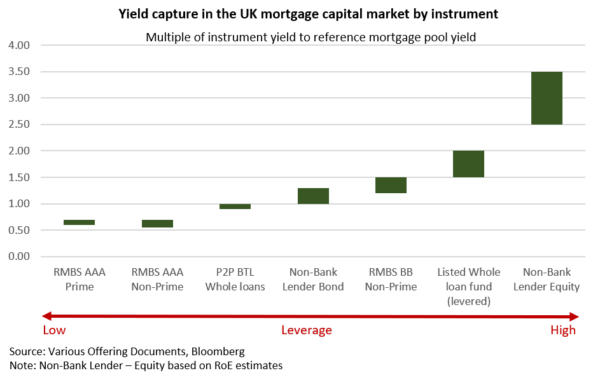

Leverage financing in itself of course mirrors the channels for debt investing into the specialist loan markets, which can range from public bond and securitization markets to private, often bilateral, facilities ranging from direct asset financing to forward flow loan purchase agreements. Within the former public markets, asset-backed securities tend to dominate, indeed the widespread use of securitization as a term financing / leverage outlet for owners of such loan books is testament to the leverability of these loan types.

Private financing agreements have become more common in recent years – from what we can tell such facilities are typically priced at appreciable spread pick-ups to public equivalent securitizations, which – judging from recent clearing spreads – typically equate to weighted average yields of 2.5-3.5% (depending on asset type) for the investment grade component of ABS/ RMBS capital structures

Understanding the risks to specialist loan book returns

Based on our simplistic analysis where annual loan book returns are a function of yield (and fee) carry less credit losses, it follows that any risks to such returns comprise factors that could potentially influence yields and/ or loss performance over the longer term. Among such factors, we would highlight the following:

- We think a key risk to loan yield resiliency – and indeed the sustainability of origination volumes – is the scope for further regulatory reform, which have already had an influential role in moderating lending rates and volumes in certain high cost consumer credit sectors. More regulation is still to come targeted mainly at the niche rather than established specialist lending markets

- Yet another key risk is the potential reintermediation of such markets by mainstream banks, fuelled – not least – by institutions that are generally flushed with capital trapped by contemporary ringfencing rules. This trend looks to be taking hold already in some parts of the first charge specialist mortgage market. Any lending ‘creep’ among specialist lender incumbents into riskier borrower markets, either because of such competition from deposit-takers and/ or other profitability pressures, could also of course shape the loss experienced by such lending in the future

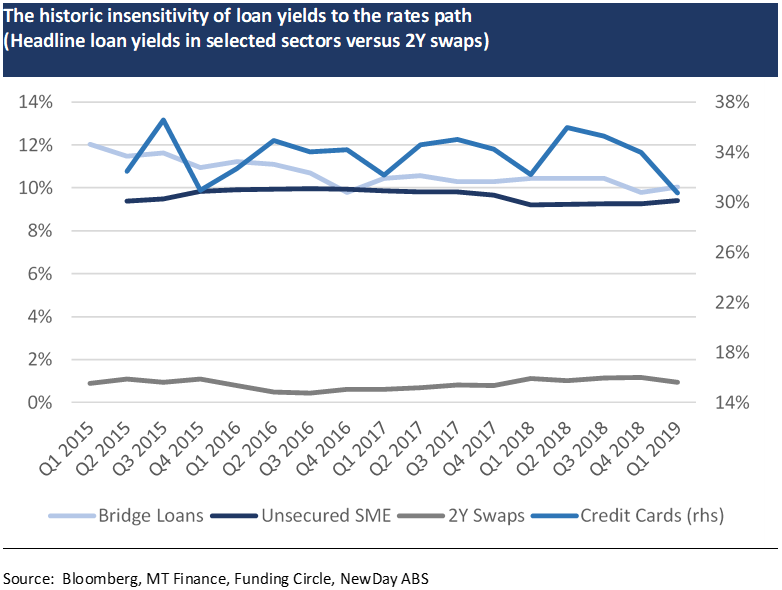

- Unlike more mainstream loan markets, the path of interest rates can be shown to be a relatively insignificant influence on loan yields – which are mostly priced with significant headroom to rates – in all but the most defensive alternative lending segments such as first charge mortgages. For the same reason, we see the credit impact of any adverse interest rate shifts being limited mostly to mortgages (if at all) given both the typically long-term debt burdens and tighter relationship to base rates. By contrast, the high yield characteristics of most other alternative lending products, not to mention the typically high turnover (or short tenor) nature of such loans, arguably makes credit performance less sensitive to policy rates in any but the most prolonged or severe of tightening cycles

- Losses are of course vulnerable to cyclical downturns or shocks. A full analysis of loss vulnerability is outside the scope of this high-level report, however we would highlight employment and disposable incomes as powerful predictors of loan performance in most alternative consumer finance markets. (Indeed, an analysis by the BoE Financial Stability Report in June 2017 found a meaningful correlation between consumer credit losses and unemployment, lagged 12 months)

- Borrower “willingness-to-pay” is also an important consideration in terms of credit performance, particularly among the high cost consumer credit sectors. Non-economic factors are relevant in this respect, which can range in our view from cases of dissatisfaction with goods purchased via credit (to include examples of say loans secured against used cars or white goods) to other forms of strategic defaulting among high cost borrowers given lender failures and/ or changes in borrower behaviour towards loan rates seen as usurious or predatory. (As a case in point, complaints related to payday loans rose five-fold in the past year, according to Resolver, an independent complaints website)

- Losses can also be influenced of course by the quality of loan servicing and delinquency workouts at the lender or servicer level. The benign cycle recently has not provided any meaningful test of workout capabilities among the current breed of lenders, many of which only emerged in the post-crisis era.

Mapping Investment Opportunities in Tradable and Unlisted Markets

Institutional investment into UK alternative lending assets prior to the crisis was limited largely to securitization capital markets, whereas today the opportunity presents itself across listed stocks/ loan investment trusts and unlisted “opportunity” funds, whole loans (via marketplace platforms mostly) as well as securitized products and other debt types: –

- Listed equity opportunities are represented via the stocks of selected larger lenders as well as listed loan funds (or closed-end investment trusts, to be exact) managed by institutional investors. Listed loan funds typically invest in a broader array of opportunities via a mix of loans as well as securities, but – with a few exceptions – tend still to be bucketed by type, for example, online/ P2P loans or real estate assets or other single-sector exposures such as SME direct lending

- Securitizations of specialist loan books dominate the debt capital markets, especially of course in established lending markets such as mortgages, autos and credit cards. A few lenders also issue bonds directly, secured via floating charges over substantially all of the unencumbered assets of the lender – such bonds span low investment grade (sold into retail markets often) to high yield (institutional). Debt issuance in any form, which serve also as a leverage tool, tends to be limited to the more established lenders with sizable loan books and origination flows

- Whole loans feature as a newer investable channel courtesy of P2P/ marketplace platforms, the vast majority of which emerged over the post-crisis era. Such loans tend to be in specific sectors such as SME or consumer or property lending, with platforms having a more diversified product suite being rarer

- Unlisted institutional funds, often structured as locked-up, PE style vehicles. Investments by managers in this regard can include debt (whole loans, asset financing, etc) and equity (loan book residuals and/or stakes in fincos). For the most part, investments in UK specialist lending among such unlisted funds are part of broader private market strategies, commonly carrying such brands as alternative or tactical opportunities, principal finance, and so on. We only know of a very few select funds that are dedicated to such specialist lending markets.

Investable capital market opportunities related to UK specialist lending – whether listed lender stock, bonds or securitized products – do not look to fully capture the loan book return economics outlined earlier. This is unsurprising in the context of liquidity premiums implicit in such traded instruments, that aside such term debt or permanent capital is usually associated with more mature lending models. With the exception of securitized residuals, asset-backed bonds across senior and mezzanine capital structures, for instance, yield noticeably lower than the whole loan equivalents. Sub-investment grade lender bonds, commonly priced in the 7-9% area, are similar in that respect. Stocks in listed lenders have generally underperformed from a total return perspective in recent years, with loan book economics heavily outweighed by lender-specific event risks. All that said, we would note that certain risk assets related to specialist lending – such as high yield or securitized bonds – look cheap versus their traded peers.

Private market, illiquid alternatives such as whole loans (via marketplace platforms) and managed loan funds appear to better capture the return economics inherent in specialist loan books, in our view. Buying whole loans via marketplace platforms is an entirely new investing format, as is (largely) investing via loan funds. Marketplace whole loans can yield anywhere between 5% to upwards of 10%, depending on both credit risk categories and asset type, with consumer loans in the lower end and SME risk in the higher end, generally. (This simple observation ignores potential loss risks in such loans of course).